White House Charts New Course for Digital Asset Policy

The White House released its comprehensive Digital Asset Policy Report (Report), fulfilling a mandate from Executive Order 14178 signed by President Donald Trump on January 23.[1] The order established the President’s Working Group on Digital Asset Markets within the National Economic Council and gave it 180 days to develop regulatory and legislative recommendations that would advance pro-innovation digital asset policies. The Report continues the administration’s emphasis on developing digital assets and related technologies in the United States. Specifically, the Report addresses, among other things, banking supervision, market structure, international competitiveness and implementation of a national digital asset stockpile from seized cryptocurrencies. The Report provides specific recommendations to federal agencies while acknowledging that many changes will require legislation.

Banking Regulators Told to Restart Crypto Programs

According to the Report, federal banking regulators should restart crypto innovation programs that were previously suspended and establish clear approval processes for custody services, trading facilitation, and other digital asset operations.[2] Banking agencies should adopt technology-neutral risk management that treats digital asset activities fairly.

Capital requirements should “accurately reflect the risk of the asset or activity” rather than the blanket higher capital charges that have effectively discouraged bank participation in digital asset markets. The Report also calls for clearer guidance for institutions seeking bank charters or Federal Reserve master accounts for digital asset business lines, and directs regulators to stop discriminating against lawful digital asset businesses.

SEC and CFTC Should Immediately Act on Crypto

The Report urges the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) to “immediately enable the trading of digital assets at the federal level” using existing authorities. Since this does not require new legislation, the agencies could act on this recommendation in a relatively short time frame.

More ambitious reforms would require legislation. The Report supports the Digital Asset Market Clarity Act of 2025 (CLARITY Act), which recently passed the House, calling it an “excellent foundation” for digital asset market structure. The CLARITY Act would grant the CFTC clear authority over spot markets in non-security digital assets while allowing SEC and CFTC registrants to engage in multiple business lines under streamlined licensing.

The Report addresses decentralized finance (DeFi) and recommends that regulators evaluate protocols based on four specific factors: 1) whether the software exercises “control” over assets; 2) whether it is technologically capable of being modified; 3) whether it operates with a centralized structure or management; and 4) whether it is logistically capable of complying with current regulatory obligations.

Stablecoins Receive Priority Treatment Under GENIUS Act

The Report calls for expeditious implementation of the GENIUS Act, which was signed into law in July and establishes a regulatory framework for payment stablecoins and their issuers.[3] The Report emphasizes three key aspects of the GENIUS Act that it considers “essential to enabling growth and stability in the digital asset market”: stablecoins must be backed by high-quality, liquid assets, issuers must obtain US licensing for domestic offerings, and the law allows US authorities to grant reciprocity to foreign jurisdictions with comparable regulatory regimes.

The Report maintains firm opposition to central bank digital currencies, recommending support for legislation like the Anti-CBDC Surveillance State Act, which passed the House in July 2025. This distinguishes the US approach from other major economies that are exploring government-issued digital currencies.

Bitcoin Reserve Implementation Details Revealed

The Report provides implementation details for the Strategic Bitcoin Reserve (SBR) and Digital Asset Stockpile (DAS), which were established by Executive Order 14233 in March 2025.[4] The Department of the Treasury has delivered initial considerations to the White House regarding the establishment and management of these holdings and will coordinate next steps to operationalize them.

The SBR and DAS serve distinct purposes with different operational parameters. The SBR treats bitcoin as reserve assets of strategic national importance and will maintain bitcoin holdings as a long-term store of value that will not be sold. The US Treasury and Commerce Departments are developing budget-neutral strategies to acquire additional bitcoin for the SBR without imposing taxpayer costs.

The DAS encompasses all other digital assets obtained through forfeiture, with Treasury retaining discretion to determine strategies for responsible stewardship of these assets. Unlike the SBR, the DAS cannot acquire additional assets beyond those obtained through forfeiture proceedings.

The Report explains that existing forfeiture programs will continue unchanged, with digital assets still used for victim compensation, law enforcement operations, and state sharing as required by statute.

[1]See Katten’s Quick Reads coverage of Executive Order 14178 here.

[2]See Katten’s client advisory on this topic here.

[3]See Katten’s client advisory on the GENIUS Act here.

[4]See Katten’s Quick Reads coverage of Executive Order 14233 here.

The [President’s Working Group on Digital Asset Markets] encourages the Federal government to operationalize President Trump’s promise to make America the “crypto capital of the world” and adopt a pro-innovation mindset toward digital assets and blockchain technologies.

United States: Going for Two! SEC Approves Multi-Crypto Asset ETP

On 29 July 2025, the US Securities and Exchange Commission (SEC) approved a proposed rule change to list and trade shares of a multi-crypto asset exchange-traded product (ETP), under NYSE Arca Rule 8.201-E. This marks the first time that the SEC has approved the listing of an ETP that will invest in more than one type of crypto asset on a spot basis; until now, the SEC has only approved listing rules permitting single crypto asset ETPs to be listed. The approved multi-crypto asset ETP (the Trust) will invest in both bitcoin and ether on a spot basis.

In approving the proposed rule change, the SEC noted that it was consistent with the Securities Exchange Act of 1934 (Exchange Act) and rules and regulations thereunder applicable to national securities exchanges. Specifically, the SEC determined it was consistent with:

Section 6(b)(5) of the Exchange Act, which requires, among other things, that the rules of an exchange be designed to “prevent fraudulent and manipulative acts and practices” and “in general, to protect investors and the public interest;” and

Section 11A(a)(1)(C)(iii) of the Exchange Act, which sets forth Congress’ finding that it is in the public interest and appropriate for the protection of investors and the maintenance of fair and orderly markets to assure the availability to brokers, dealers, and investors of information with respect to quotations for and transactions in securities.

The SEC concluded that, for purposes of the foregoing, the Trust was substantially similar to other spot crypto ETP proposals that the SEC previously approved, including with respect to the Trust’s structure, terms of operation, trading of shares, representations of the exchange listing the shares, pricing information availability, portfolio holdings transparency, and types of surveillance procedures.

We anticipate additional rule change approvals in the near future, as exchanges have submitted similar applications on behalf of other multiple crypto asset ETPs. This approval is one more step in the US towards treatment of crypto asset ETPs in the same manner as traditional exchange traded products.

United States: In Cash or In-Kind—EC Approves Options for Creations and Redemptions of Crypto ETP Shares

On 29 July 2025, the US Securities and Exchange Commission (SEC) issued an order approving proposed rule changes to permit various exchange-traded products (ETPs) to engage in creations and redemptions of their shares with authorized participants (APs) on an in-kind basis. The proposed rule changes were submitted by the Nasdaq Stock Market LLC, Cboe BZX Exchange, Inc. and NYSE Arca, Inc. (Exchanges) with respect to the ETPs seeking to engage in in-kind creations and redemptions.

In approving the proposed rule changes, the SEC determined that they would be consistent with federal securities laws, specifically with Section 6(b)(5) of the Securities Exchange Act of 1934, which requires that rules adopted under that statute be designed to, among other things, prevent fraudulent and manipulative acts and practices, promote just and equitable principles of trade, and generally protect investors and the public interest.

This decision marks a shift in policy by the SEC from the initial approvals of spot bitcoin and spot ether ETPs, which were restricted to cash-based creations and redemptions. Under the rule changes, the ETPs will be able to transact with APs in cash and engage in creations or redemptions of their shares in an in-kind transaction of spot bitcoin or spot ether, as necessary or desired. Permitting in-kind creations and redemptions may enhance tax efficiencies and minimize transaction costs for the ETPs (and thus shareholders), as well as provide market participants with flexibility. Importantly, in applying for the rule changes, the Exchanges represented that all other representations relating to the ETPs contained in the initial approvals will remain unchanged and continue to constitute continuing listing standards. The SEC’s approval of in-kind creations and redemptions allows the ETPs to operate more like traditional exchange traded products.

Treasury Postpones Effective Date of Investment Adviser AML Rule

On July 21, the US Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) announced a two-year postponement of the Anti-Money Laundering (AML)/Countering the Financing of Terrorism (CFT) Program and Suspicious Activity Report filing requirements for registered investment advisers (IAs) and exempt reporting advisers.

The rule, originally scheduled to take effect on January 1, 2026, will now become effective on January 1, 2028.

We previously reported on the final rule issued on August 28, 2024, here.

The IA AML rule was developed to address illicit finance risks and vulnerabilities in the IA sector, particularly those posed by criminals and foreign adversaries seeking to exploit the US financial system. However, FinCEN has acknowledged the need to ensure that AML requirements are appropriately tailored to the diverse business models and risk profiles of IAs. The postponement is intended to:

Balance regulatory costs and benefits.

Allow for further tailoring of the rule to accommodate the varied structures and risk profiles of IAs.

Reduce potential compliance costs and regulatory uncertainty for industry participants.

Regulatory Developments and Next Steps

During the extended period, FinCEN will revisit the substance and scope of the IA AML rule through a new rulemaking process. In addition, FinCEN, in coordination with the US Securities and Exchange Commission (SEC), intends to reconsider the joint proposed rule regarding customer identification program requirements for IAs. The agency will provide regulatory certainty to the sector by issuing appropriate exemptive relief to formally delay the effective date.

Despite the delay in domestic rulemaking, FinCEN and other US authorities continue to prioritize AML and sanctions enforcement, particularly with respect to foreign threats and sanctions violations. Recent enforcement actions have emphasized the importance of AML and sanctions compliance programs, especially for IAs with cross-border activities or high-risk counterparties. IAs should remain vigilant regarding their AML and sanctions compliance obligations, and consider maintaining or enhancing voluntary AML programs in line with industry best practices and evolving enforcement priorities.

Key Takeaways

The effective date for the IA AML rule is postponed from January 1, 2026, to January 1, 2028.

FinCEN will review and potentially revise the rule to better address the unique characteristics and risk profiles of IAs.

The agency will coordinate with the SEC on related customer identification program requirements.

IAs should continue to monitor regulatory developments and consider maintaining or enhancing voluntary AML and sanctions compliance programs, particularly in light of ongoing enforcement activity and the evolving regulatory landscape.

HMRC Publishes Draft Legislation for New UK Carried Interest Tax Regime

Background

On July 21, 2025, HM Revenue and Customs (HMRC) published the long-awaited draft legislation (Draft Legislation) for the new UK carried interest tax regime (New Regime) that will apply from April 6, 2026. Under the New Regime, carried interest that would previously have been taxed as capital gain will instead be treated as trading income and subject to income tax and Class 4 National Insurance contributions (NIC) for any carried interest arising from that date.

The Draft Legislation was introduced following a long period of consultation between HMRC, HM Treasury and industry. Publication of the Draft Legislation marks the start of an eight-week technical consultation on the legislation, running until September 15, 2025. The purpose of the technical consultation is to resolve any drafting inconsistencies or other necessary amendments for the legislation to work as intended; the commercial principles underlying the new carried interest taxation are now effectively set.

Who is likely to be affected

The New Regime will impact individuals who receive carried interest, where either the individual is a UK tax resident at the time of receipt or the carried interest relates to investment management services performed in the United Kingdom by a non-UK resident where the individual meets certain conditions. There is no grandfathering under the New Regime for carried interest awarded prior to April 6, 2026, so from that date, capital gains treatment for carried interest receipts is simply no longer available.

Main features of the new regime

In line with the current carried interest tax regime, the New Regime applies where an individual performs investment management services directly or indirectly in respect of an investment scheme (i.e., an Alternative Investment Fund or a collective investment scheme —see further below) under any arrangements and a sum of carried interest arises to the individual under those arrangements. As stated above, the Draft Legislation provides that the individual is treated as carrying on a trade, and carried interest (less any permitted deductions) is treated as the profits of that trade.

The principal division of carried interest taxation into two tax regimes is retained: carried interest that does not satisfy the 40-month investment portfolio holding requirement — previously income-based carried interest and now termed “Non-Qualifying Carried Interest” under the Draft Legislation — remains subject to full income tax and NIC. Carried interest that does meet the 40 months portfolio holding period and other applicable conditions will be classified as “Qualifying Carried Interest” subject to a special rate of tax: the new legislation will provide that carried interest (subject to limited permitted deductions) is treated as trading profits for tax purposes but Qualifying Carried Interest (less deductions) is subject to a multiplier of 72.5 percent, whereas Non-Qualifying Carried Interest is not. Under the current highest income tax rate of 45 percent and NIC of 2 percent, the 72.5 percent multiplier would result in an effective 34.1 percent combined tax and NIC rate for Qualifying Carried Interest (less permitted deductions).

The Draft Legislation includes detailed provisions for determining the average holding period of an investment scheme and has specific provisions relating to the time of acquisition of various types of investment, which are similar to the provisions in the current income-based carried interest rules in the disguised investment management fee legislation. The main change is that the Draft Legislation treats credit funds generally in the same way as other funds.

Under the Draft Legislation, the definition of carried interest remains based on characteristics (very broadly, considering the priority waterfalls of payment for investors and circumstances under which carried interest holders are permitted to participate). However, the scope of “investment schemes” has been expanded to include Alternative Investment Funds (AIFs), i.e., non-retail investment funds established as corporate entities and that qualify as “Alternative Investment Funds” for the purposes of the Alternative Investment Fund Managers Regulations 2013. The definition was previously limited to investment funds defined as collective investment schemes under section 235 of the Financial Services and Markets Act 2000 — which applied to most investment schemes but had a specific exclusion for closed-ended corporate funds. A driving factor behind the expansion to include AIFs is the availability of the lower carried interest tax rate for such corporate arrangements; however, the corporate inclusion is not necessarily positive for all arrangements.

A further change is the introduction of the asset-level average holding period for employment-related securities from April 6, 2026; employment-related securities are excluded from current income-based carried interest rules but will be included within the Non-Qualifying Carried Interest rules under the New Regime.

Exclusive regime and double taxation

Generally, carried interest will only be chargeable to income tax under the New Regime and not subject to income tax under any other provisions. However, if a tax charge arises in respect of carried interest under section 62 (earnings) or Part 7 (employment income related to securities) of the Income Tax (Earnings and Pensions) Act 2003, that income tax charge will still stand, but the individual may make a claim for the carried interest charge under the New Regime to be adjusted to prevent double taxation. The relief given is that which is “just and reasonable,” rather than pound for pound. The New Regime does not, however, deliver an “exclusive regime” as was originally proposed. Double tax relief is similarly available where UK tax has been charged on another person in relation to the same carried interest. However, there is no express double tax relief in respect of non-UK tax, but double tax treaty relief may be available, depending on the terms of the treaty. The election to charge carried interest to tax as it arises, rather than when received under the current regime, is also included in the Draft Legislation under the New Regime to allow individuals who are taxable on carried interest in the United Kingdom and another jurisdiction to align the timing of the tax charges in order to facilitate double tax treaty claims. As carried interest will be trading profits under the New Regime, the relevant treaty article is likely to be the business profits article, but that may not align with the other jurisdiction’s treatment of carried interest. Therefore, the ability to claim double tax treaty relief is uncertain under the New Regime.

As described above, the New Regime retains a significant number of principal features that were present in the current legislation. The Draft Legislation also sets out the circumstances in which carried interest is deemed to arise to an individual where it actually arises to another person — which are equivalent to the current rules under the disguised investment management fee regime. In addition, numerous anti-avoidance provisions will still apply where arrangements are entered into in order to fall within certain provisions of the regime.

HMRC concessions

The Draft Legislation also reflects the Government concessions made in the policy update from June 5, 2025, on the carried interest tax reform, which were the subject of prolonged discussion between HM Treasury and industry and ultimately accepted as too difficult to introduce. Specifically:

There will no minimum co-investment requirement or minimum carried interest holding period condition.

The geographical scope of the New Regime has been reduced, so that UK investment management services performed by a non-resident individual in a tax year do not give rise to UK tax where such services do not exceed 60 UK working days (broadly defined as three hours of work performed in the United Kingdom on a given day).

UK resident individuals leaving the United Kingdom will not be subject to UK tax on their carried interest payment if three full tax years (in addition to the current tax year) have passed, during which the individual was neither UK tax resident nor met the above 60 UK workday threshold.

Conclusion

The Draft Legislation is clearly set out, although there are likely to be some technical changes following the consultation period. It also clarifies certain areas that are uncertain under the current legislation. The Government’s June climbdown on aspects, including abandoning the requirement for managers to pay for their carried interest award and foregoing a minimum carried interest holding period at manager level, removed some of the key sticking points.

Going forward, it will be simpler for taxpayers under the New Regime to apply the rules for carried interest, as it will be solely within the income tax regime rather than split between capital gains tax and income tax as it is currently (assuming that in either case, the tax rate for carried interest would have been set at the same level regardless of which tax regime applies).

Payment Stablecoins Get “Smart” (or GENIUS-like)

Congress recently passed the first significant federal legislation recognizing the apparent enduring presence of payment stablecoins in the US financial and consumer markets. President Donald Trump signed into law on July 18, the Guiding and Establishing National Innovation for US Stablecoins Act or the GENIUS Act1, which establishes a US state and federal regulatory framework for “payment stablecoins” (i.e., US dollar-backed stablecoins) and their issuers, and also confirms that payment stablecoins are not securities under the federal securities laws or commodities under the Commodity Exchange Act. The GENIUS Act charges state and federal banking regulators with overseeing payment stablecoin issuers.

The GENIUS Act, a hallmark of Congress’s and the current administration’s efforts to support digital assets, stablecoins and cryptocurrencies, benefited from bipartisan support, passing the Senate by a vote of 68 to 30 and the House of Representatives by a vote of 308 to 122. The law becomes effective on the earlier of (i) 18 months after its passage (January 18, 2027), or (ii) 120 days after final regulations are issued. Regulations implementing the GENIUS Act must be issued within one year of enactment.

What Qualifies As a Payment Stablecoin?

The GENIUS Act generally defines a “payment stablecoin” as a digital asset that is or is designed to be used as a means of payment or settlement, which the issuer:

is obligated to convert or repurchase for a fixed monetary value, not including a digital asset denominated in a fixed amount of monetary value; and

represents will maintain or “creates a reasonable expectation that it will maintain” a stable value relative to the value of a fixed amount of monetary value.

In short, for purposes of the GENIUS Act, payment stablecoins must be pegged to a defined unit of monetary value (such as the US dollar) and be supported by adequate reserves.

Importantly, the GENIUS Act clarifies the regulatory status of payment stablecoins by amending the federal securities laws and the Commodity Exchange Act (CEA). Specifically, under the GENIUS Act, a payment stablecoin issued by a permitted payment stablecoin issuer (PPSI) is excluded from the definition of a “security” under the Securities Act of 1933, the Securities Exchange Act of 1934, the Investment Company Act of 1940 (the 1940 Act), the Investment Advisers Act of 1940 (the Advisers Act), and the Security Investor Protection Act of 1970. Payment stablecoins are also excluded from the definition of “commodity” under the CEA.

As a result of these status determinations by Congress, a PPSI does not need to register as an “investment company” solely because it issues payment stablecoins. However, issuers of other types of stablecoins, such as certain foreign issuers that do not meet the GENIUS Act’s requirements, need to consider whether the 1940 Act applies. Additionally, the GENIUS Act has potential implications for investment adviser registration, as payment stablecoins are not securities, so persons providing advice exclusively about such stablecoins would not be considered investment advisers under the Advisers Act.2

Similarly, with respect to the authority of the Commodity Futures Trading Commission (CFTC), the GENIUS Act’s status determinations mean that futures contracts, swap contracts and other derivatives on permitted payment stablecoins cannot be offered under the CEA, as such instruments require the underlying asset to be classified as a “commodity.”

Who Can Issue Payment Stablecoins?

The GENIUS Act establishes a US state and federal regulatory framework for “payment stablecoins” and their issuance in the United States by PPSIs and qualifying foreign issuers. The GENIUS Act provides different paths for three types of PPSIs. The following table outlines the three PPSIs and their pathways:

PPSI

Regulatory Agency that Licenses,3 Supervises and Examines the PPSI and the Payment Stablecoins

PATH 1:

Subsidiary of an insured depository institution

Primary Federal Payment Stablecoin Regulator, which is dependent upon the charter type of the affiliated insured depository institution:

Office of the Comptroller of the Currency (OCC) – national banks and federal savings associations4

Board of Governors of the Federal Reserve System (FRB) – state-chartered member banks and foreign bank branches, and agencies

Federal Deposit Insurance Corporation (FDIC) – state nonmember banks

National Credit Union Administration (NCUA) – federal- and state-chartered credit unions

PATH 2:

Federal qualified payment stablecoin (includes uninsured national banks chartered by the OCC and federal branches of foreign banks)5

OCC

PATH 3:

State qualified payment stablecoin

A state payment stablecoin regulator (i.e., a state agency that has primary regulatory and supervisory authority in the state over payment stablecoin issuers)

Core Regulatory Requirements for All PPSIs

Reserve Requirements. All PPSIs are required to maintain identifiable reserves backing the issuer’s payment stablecoins outstanding on an at least 1:1 basis. These reserves must comprise specified high-quality, liquid assets, including US coins and currency, demand deposits at insured depository institutions, Treasury bills with remaining maturity of 93 days or less, certain repurchase agreements, and government money market funds invested solely in these underlying assets.

Disclosure and Reporting. PPSIs must publicly disclose their redemption policy, establishing clear and conspicuous procedures for the timely redemption of outstanding payment stablecoins and publicly disclose all fees associated with purchasing or redeeming the payment stablecoins. No less than seven days’ prior notice to consumers is required before such fees can be changed. Additionally, PPSIs must publish the monthly composition of their reserves on their website, including the total number of outstanding payment stablecoins issued and the amount and composition of the reserves, including the average tenor and geographic location of custody of each category of reserve instruments.

Monthly Certification. A registered public accounting firm must examine this monthly information, and the Chief Executive Officer and Chief Financial Officer of a PPSI must submit a monthly certification as to the accuracy of the monthly report to either the primary federal payment stablecoin regulator or the state payment stablecoin regulator. Any person who submits a false certification is subject to criminal penalties under federal law.

Additional Regulatory Standards. The primary federal payment stablecoin regulators (i.e., the OCC, FRB and the NCUA), or in the case of state qualified payment stablecoin issuers, the state payment stablecoin regulator, must issue regulations implementing capital requirements, liquidity standards, reserve asset diversification requirements, and operational, compliance, and information technology risk management standards, including Bank Secrecy Act and sanctions compliance standards. These requirements must be tailored to the business model and risk profile of PPSIs and may not exceed sufficient standards to ensure the ongoing operations of PPSIs.

With respect to these regulatory requirements, the OCC, the FRB, the FDIC, and the NCUA are permitted to prescribe standards to tailor or differentiate among issuers on an individual basis or by category, taking into consideration certain defined variables.6 The same agencies are also required to examine the PPSIs they charter to assess the nature of the licensee’s operations and financial condition, as well as the financial, operational and technological risks the PPSI poses to its safety and soundness and the stability of the US financial system.

Permitted and Prohibited Activities

Permitted Activities. PPSI activities are limited to: issuing payment stablecoins; redeeming payment stablecoins; managing related reserves; providing custodial or safekeeping services for payment stablecoins; and undertaking other functions that directly support these core activities. The GENIUS Act provides that it is unlawful to market a product in the United States as a “payment stablecoin” unless the product is issued pursuant to the GENIUS Act.

Prohibited Activities. The GENIUS Act specifically prohibits certain activities by PPSIs. PPSIs may not provide services to a customer on the condition that the customer obtains an additional paid product or service from the PPSI, or any of its subsidiaries, or agrees not to obtain an additional product or service from a competitor. PPSIs and foreign payment stablecoin issuers may not pay the holder of any payment stablecoin “any form of interest or yield” solely in connection with the holding, use, or retention of the payment stablecoin. PPSIs also may not use any combination of terms relating to the US Government in the name of a payment stablecoin or market a payment stablecoin in such a way that a reasonable person would perceive the payment stablecoin to be legal tender, issued by the United States, or guaranteed or approved by the US Government.

Exempt Transactions. The GENIUS Act exempts transactions involving the direct transfer of digital assets between two individuals that do not use an intermediary, transactions involving US residents that own digital assets in accounts held at the same company both in the United States and abroad, and transactions involving digital wallets that hold digital assets.

Application Process and Special Rules

The GENIUS Act enumerates the factors that a primary federal payment stablecoin regulator must evaluate to issue a PPSI license. Those factors include the points highlighted in “Core Regulatory Requirements for All PPSIs” above. Decisions with respect to applications must be provided to the applicant no later than 120 days after the application is “substantially complete,” and the failure to provide a decision on a “complete” application within the 120-day period means that the application is deemed approved.

Public companies (i.e., those required to file reports under the Securities Exchange Act of 1934) that are not predominately engaged in one or more financial activities may not issue a payment stablecoin unless such company receives a unanimous vote from the Stablecoin Certification Review Committee (which is comprised of the US Treasury Secretary, the Chair of the FRB, and the Chair of the FDIC) upon such Committee’s finding that certain statutory requirements have been satisfied.

State-Level Regulatory Framework

The GENIUS Act provides a pathway for state-level regulation of payment stablecoin issuers, but with significant limitations and federal oversight. The state-level regime of licensing, examining, and supervising payment stablecoin issuers is only available: (i) to entities with a consolidated total outstanding issuance of not more than $10B (the State Cap); and (ii) in instances where the state-level regulatory regime is “substantially similar” to the federal regulatory framework, with such determination made pursuant to a framework established by the US Treasury Secretary.

Certification Process. The applicable state agency must submit an initial certification to the Stablecoin Certification Review Committee attesting that the applicable state regime meets this required standard. Annual recertifications are also required, although the Stablecoin Certification Review Committee possesses certain rights to deny recertification.

Federal Transition Requirements. To the extent a state qualified payment stablecoin issuer that is an insured depository institution exceeds the State Cap, it must transition to the federal regulatory framework of the primary federal payment stablecoin regulatory framework of the state-chartered depository institution, which framework will be administered jointly by such state payment stablecoin regulator and the primary federal payment stablecoin regulator. Other institutions that exceed the State Cap must transition to the federal regulatory framework administered by the state payment stablecoin regulator and the Comptroller of the Currency.7

Federal Oversight Authority. State qualified payment stablecoin regulators may enter into a memorandum of understanding (MOU) with the FRB by which the FRB may “participate” in the supervision, examination and enforcement of the GENIUS Act with respect to state qualified payment stablecoin issuers in such state. Regardless of the existence of an MOU, however, state qualified payment stablecoin regulators and the FRB “shall share” information on an ongoing basis related to state qualified payment stablecoin issuers.

In addition, the FRB may issue orders against a state qualified payment stablecoin issuer or its institution-affiliated party when circumstances that are “unusual and exigent” exist, but only if the FRB has first provided 48 hours’ prior written notice to the applicable state payment stablecoin regulator. Similar authority is provided to the Comptroller of the Currency concerning state qualified payment stablecoin issuers that are nonbank entities.

Bank Secrecy Act and AML Requirements

The GENIUS Act designates PPSIs as “financial institutions” under the Bank Secrecy Act (BSA). The BSA imposes recordkeeping and reporting requirements on such entities to deter and detect money laundering, terrorist financing and other illicit financial activities. Financial institutions must report any suspicious activity that might indicate money laundering, tax evasion, or other criminal activity. The BSA also requires that financial institutions adopt an anti-money laundering (AML) program that is reasonably designed to deter and detect money laundering and includes a designated compliance officer, ongoing employee training and independent audits. As part of its AML program, a financial institution must adopt policies and procedures to form a reasonable belief about the true identity of its customers.

The GENIUS Act also provides that the US Treasury Secretary, to the best of their ability, will coordinate with PPSIs before blocking and prohibiting transactions in property and interests in property of a foreign person, although the Secretary has no obligation to notify the PPSI before doing so.

All PPSIs, regardless of the type of charter, are required to submit annual certifications to their associated regulator setting forth an attestation that the PPSI has implemented an AML and economic sanctions program that is reasonably designed to prevent the PPSI from facilitating money laundering.

Foreign Payment Stablecoin Issuers

The GENIUS Act establishes a framework for foreign payment stablecoin issuers to offer payment stablecoins in the United States, subject to specific requirements and regulatory oversight. Foreign payment stablecoin issuers may offer payment stablecoins in the United States if they are subject to regulation and supervision by a foreign payment stablecoin regulator in a jurisdiction with a regulatory regime that the US Treasury Secretary determines is “comparable” to the US framework established under the GENIUS Act, register with the OCC, hold reserves in a US financial institution sufficient to meet liquidity demands of US customers, and are not domiciled in a country subject to comprehensive US economic sanctions or designated as a jurisdiction of primary money laundering concern.

The US Treasury Secretary may determine whether a foreign jurisdiction has a comparable regulatory regime only upon recommendation from each Stablecoin Certification Review Committee member and must publish a justification for such determinations in the Federal Register. If a foreign payment stablecoin issuer fails to comply with lawful orders, Treasury may designate the issuer as “noncompliant” and, after a 30-day cure period, prohibit digital asset service providers from facilitating secondary trading of such payment stablecoins in the United States. Civil monetary penalties of up to $1,000,000 per violation per day may be imposed on non-compliant foreign payment stablecoin issuers.

Custody Requirements

The GENIUS Act establishes comprehensive custody requirements for entities providing safekeeping services for payment stablecoin reserves, payment stablecoins used as collateral, and private keys used to issue payment stablecoins. Only certain regulated entities may provide custodial or safekeeping services for payment stablecoin reserves and related assets, specifically those subject to supervision or regulation by a primary federal payment stablecoin regulator or other primary financial regulatory agency under the Dodd-Frank Wall Street Reform and Consumer Protection Act, or by a state bank supervisor or state credit union supervisor that makes available to the FRB information that the Board determines necessary and relevant.

Custodians must treat payment stablecoins, private keys, cash and other customer property as belonging to the customer and not as property of the custodian. They must take appropriate steps to protect customer assets from creditor claims. Customer property must be separately accounted for and segregated from the custodian’s own assets, though the GENIUS Act provides practical exceptions, including permitting commingling in omnibus accounts at depository institutions and allowing withdrawals necessary for transaction settlement. Customer claims against custodians have priority over other claims with respect to payment stablecoins held by the custodian, unless the customer expressly consents to a different priority arrangement.

Bankruptcy and Insolvency Protections

The GENIUS Act amends the federal bankruptcy code to provide enhanced protections for payment stablecoin holders in the event of issuer insolvency. In any insolvency proceeding of a PPSI, the claim of a person holding payment stablecoins issued by the PPSI has priority, on a ratable basis with the claims of other persons holding such payment stablecoins, over the claims of the PPSI and any other holder of claims against the permitted payment stablecoin issuer, with respect to required payment stablecoin reserves.

The GENIUS Act also provides that required payment stablecoin reserves are excluded from the bankruptcy estate of the issuer, and that the automatic stay does not prevent the redemption of payment stablecoins from payment stablecoin reserves required to be maintained under the GENIUS Act. US bankruptcy courts are required to use their best efforts to enter a final order to begin distributions to payment stablecoin holders not later than 14 days after the required hearing, provided there are payment stablecoin reserves available for distribution on a ratable basis to similarly situated payment stablecoin holders.

Transitional Provisions

Notably, through July 2028, digital asset service providers may continue to offer payment stablecoins that are not issued by PPSIs. However, payment stablecoins that are issued by entities other than PPSIs may not be treated as cash or a cash equivalent for accounting purposes, may not be acceptable as a settlement asset to facilitate wholesale payments between banking organizations, and are not eligible as cash or cash equivalent margin and collateral for futures commission merchants, derivatives clearing organizations, broker-dealers, registered clearing agencies, swap dealers and security-based swap dealers.

Market Impact and Next Steps

While the GENIUS Act provides a prescriptive framework that permits PPSIs to issue payment stablecoins, myriad issues remain in terms of widespread adoption, particularly in the consumer “use case.” For example, Automated Clearing House (ACH) and credit card payments have established guardrails and related protections for consumers who believe transactions have been impermissibly posted to their bank or credit card account. Also, credit card associations have adopted fulsome, protective measures that allow consumers to “chargeback” transactions for which there is a permissible basis or claim. The nascent nature of payment stablecoins means these protective features have not yet been developed, let alone codified and marketed to consumers in a way that supports the use of payment stablecoins as an alternative to debit cards, credit cards, or ACH bank account debits.

That said, once these types of infrastructure components are built to scale and other features of the movement to this type of payment system processing are developed, whereby merchants and consumers can feel adequately protected, the use of payment stablecoins represents a continuing, and possible existential, threat to the US banking industry. While the GENIUS Act’s prohibitions on tying and the payment of interest or yield in connection with payment stablecoin holdings provides some degree of relief to US banks, the effect the GENIUS Act has on the broad spectrum of consumer and commercial financial markets is not yet realized (and likely will not be realized until PPSIs convince their respective markets of the “use case”).

The GENIUS Act’s ultimate impact will be shaped by the implementation process that lies ahead. Regulators must issue final rules by July 18, 2026, creating crucial comment opportunities for industry participants to influence practical requirements around capital, liquidity, and operational standards. Companies should begin evaluating which regulatory pathway best suits their business model (i.e., federal qualification through the OCC, subsidiary approval, or state-level certification). Active participation in the rulemaking process through comment letters and regulatory engagement will be essential to ensure the GENIUS Act framework supports innovation and maintains appropriate consumer protections.

1 https://www.congress.gov/119/bills/s1582/BILLS-119s1582enr.xml.

2 An investment adviser, as defined in Section 202(a)(11) of the Advisers Act, generally is required to register with the SEC unless the adviser qualifies for an exemption or is prohibited from registering. Section 202(a)(11) defines “investment adviser,” in relevant part, as “any person who, for compensation, engages in the business of advising others . . . as to the value of securities or as to the advisability of investing in, purchasing, or selling securities.”

3 PPSIs that are either a subsidiary of insured depository institutions or a federal qualified payment stablecoin issuer are not subject to state licensing or chartering requirements in connection with activities undertaken in their capacity as a PPSI. The broad scope of this preemption makes it likely that many nonbanks will seek to obtain a federal qualified payment stablecoin issuer license from the OCC to leverage 50 state, unified operations offered from a single platform.

4 Federal savings associations do not need to satisfy the “qualified thrift lender” test with respect to reserves that are held pursuant to the GENIUS Act.

5 This would include uninsured trust banks. Several crypto companies have applications pending with the OCC to obtain this type of charter. This includes Ripple National Trust Bank (the public portion of the application is available at https://occ.gov/topics/charters-and-licensing/digital-assets-licensing-applications/ripple-national-trust-bank.pdf).

6 These variables include capital structure, business model risk profile, complexity, financial activities, size and any other risk-related factors the banking agency determines appropriate.

7 Note that the GENIUS Act includes a presumptive waiver from these requirements for entities that were licensed and supervised to engage in digital asset or payment stablecoin activities before the 90-day period ending on the date of enactment of the GENIUS Act, although such presumption can be defeated if certain factors are met.

Sustainability Under the Microscope: ESMA’s Reality Check

On the 30 June 2025, the European Securities and Markets Authority (“ESMA”) published its final report on the 2023–2024 Common Supervisory Action (“CSA”) on the integration of sustainability risks and disclosures. This initiative, conducted in collaboration with the European Economic Area’s national competent authorities (“NCAs”), focused on assessing compliance with the Sustainable Finance Disclosure Regulation (“SFDR”), Alternative Investment Fund Managers Directive, and the UCITS Directive.

The findings, which we summarise here alongside some useful good and poor practice examples, offer useful insights and supervisory expectations for asset managers navigating SFDR’s disclosures.

Supervisory Focus and Scope

The CSA reviewed asset managers’ approach to integrating sustainability risks, the quality of their disclosures on the integration and the likely impact at both entity and product levels.

The key areas of assessment included:

governance and risk management frameworks for sustainability risks;

consistency and clarity of SFDR disclosures;

alignment of remuneration policies with sustainability objectives; and

mitigation of greenwashing risks.

Integration of Sustainability Risks

ESMA determined that most asset managers demonstrated a baseline level of compliance with sustainability risks integrated into governance structures and investment processes. However, ESMA also identified several areas for improvement:

Policy Gaps: Some managers lacked documented procedures or escalation mechanisms for sustainability breaches.

Resource Constraints: Smaller firms often had limited dedicated ESG personnel, while larger firms showed more structured ESG integration.

Data and Methodology: Inconsistent use of ESG data and limited verification of third-party sources were common.

ESMA emphasised the need for robust internal controls, regular policy updates, and clear delineation of responsibilities across compliance, risk, and investment functions to support with the improvement of the integration of sustainability risks.

Entity-Level Disclosures

ESMA highlighted mixed quality in entity-level SFDR disclosures in its CSA:

Principal Adverse Impact (PAI) Statements: Many lacked detail or failed to explain non-consideration adequately.

Remuneration Policies: Several managers did not clearly link ESG performance to variable pay or failed to publish relevant information on their own websites.

Greenwashing Risk Management: While most firms acknowledged greenwashing risks, confusion between sustainability-related risks and greenwashing risks persisted.

ESMA recommends that asset managers enhance transparency, ensure disclosures are easily accessible, and align internal policies with public statements to support with improving entity-level disclosures.

Product-Level Disclosures

At the product level, ESMA found significant variability in how sustainability objectives and methodologies were disclosed:

Inconsistent Use of ESG Terminology: Some Article 6 funds used ESG-related names or imagery, raising greenwashing concerns.

DNSH and Good Governance: Many managers did not adequately demonstrate how investments met the “Do No Significant Harm” (“DNSH”) principle and/or good governance criteria, as relevant to a particular fund.

Sustainable Investment Thresholds: Discrepancies between committed and actual sustainable investment levels were noted.

Asset managers are urged by ESMA to ensure that disclosures are not only compliant but also meaningful and reflective of actual investment practices.

Regulatory Follow-Up and Enforcement Outlook

The NCAs were asked to report on the follow-up actions they plan to take following the CSA exercise. The majority considered that there was an overall satisfactory level of compliance among managers and most of the vulnerabilities identified were addressed before the end of the period of the CSA.

As part of this process:

many NCAs issued bilateral letters to managers outlining specific areas for improvement;

others took more formal steps, including supervisory orders, warning notices, or risk mitigation programmes; and

follow-up actions focused particularly on issues such as the incorrect use of fund names, suggestive non-textual imagery, and incomplete or missing disclosures.

Most NCAs expect these shortcomings to be resolved in the coming weeks or months. Only one NCA reported having taken enforcement action, while another indicated that enforcement was under consideration. The prevailing view among NCAs is that escalated supervisory measures are more effective than enforcement in addressing the identified breaches.

Below is a table outlining some key areas of what ESMA considers constitutes to be good and bad practice with respect to sustainability risks, both in their practical integration and disclosures:

Good Practice

Below average / Noncompliance

1. Policies and Procedures on the Integration of Sustainability Risks A fund establishes clear screening criteria and exclusion lists which are reviewed at least annually. If the portfolio becomes overly exposed to unabated fossil fuels, the manager identifies the risk and proactively rebalances the portfolio by reallocating investments to less vulnerable sectors.

2. Integration of Sustainability Risks in Risk Management Procedures The risk management framework incorporates ESG scores into existing metrics to assess the overall risk profile of the funds and portfolios under management. If a portfolio exhibits elevated ESG risk over two consecutive quarters, the manager evaluates appropriate corrective measures to enhance the fund’s ESG profile over the long term.

3. Engagement Policies One manager’s PAI statement includes a detailed explanation of how its engagement policies will be adjusted in cases where no reduction in principal adverse impacts is observed over multiple reporting periods. This reflects a proactive and ambitious engagement strategy, as envisaged under Article 8(2)(b) of the SFDR Delegated Regulation.

4. Designation of Sustainability Characteristics or Objectives The manager clearly identifies the fund’s promoted characteristics and objectives in its financial product disclosures, aligning them with recognised classifications such as specific sub-objectives under the UN Sustainable Development Goals (“SDGs”), the environmental objectives outlined in Article 9 of the Taxonomy Regulation, and the social objectives proposed in the February 2022 report by the Platform on Sustainable Finance on a social taxonomy.

5. Good Governance The manager conducted a governance screening using clearly defined criteria and principles to determine whether a company should be excluded or retained in the portfolio when a controversy arises, both at the point of investment and through ongoing monitoring. The procedures implemented for funds disclosing under Article 8 of the SFDR were deemed sufficient to ensure that investee companies adhere to good governance practices.

1. Senior Management’s Skills and Expertise Senior management lacks sufficient resources and expertise to effectively integrate sustainability risks and does not possess a demonstrable track record in sustainability supported by appropriate training.

2. Failure to Disclose Reduction of Carbon Emissions Aligned with the Paris Agreement One manager assesses the principal adverse impacts (PAIs) of its investment decisions on sustainability factors but does not reference the extent to which these align with the objectives of the Paris Agreement, despite employing a dedicated risk assessment tool to evaluate decarbonisation pathways at both asset and portfolio levels. In accordance with Article 4(2)(d) of the SFDR, the manager should provide a clear indication of how its investment strategy aligns with the Paris Agreement’s goals.

3. Good Governance Criteria The processes implemented by managers for Article 8 SFDR funds were insufficient to ensure that investee companies adhered to good governance practices. While some level of screening was in place, there were no clearly defined timeframes or materiality thresholds to determine how long engagement with non‑compliant companies could continue before exclusion from the investment universe. Under Article 8 of the SFDR, such governance standards must be upheld regardless of whether the fund qualifies as a sustainable investment.

4. Inconsistency Between Marketing Material and Pre-Contractual Disclosures A manager disclosed inconsistent information between a fund’s marketing materials and its pre-contractual documentation. While the marketing materials featured various logos and visual elements — some referencing the UN SDGs — they did not reflect any corresponding commitments or characteristics in the fund’s pre-contractual disclosures. This discrepancy contravenes Article 13 of the SFDR, which requires that marketing communications must not contradict the information provided under SFDR disclosures.

5. Identification of Excessive Numbers of Characteristics and Objectives In its pre-contractual disclosures, a fund claims to promote all of the UN SDGs as part of its sustainability characteristics. However, in subsequent periodic disclosures, it reports contributions to only one or two of those goals. This approach does not provide meaningful guidance to investors regarding the fund’s investment strategy and may instead allow for retrospective justification of investments by loosely associating them with broad sustainability objectives.

What can asset managers do to address these potential risks?

The CSA has underscored the importance of credible, transparent, and verifiable sustainability practices in asset management and again put managers on alert that NCAs are actively supervising SFDR’s requirements and broader sustainability-related claims.

SEC Approves In-Kind Creations and Redemptions for Crypto ETPs

On July 29, 2025, the U.S. Securities and Exchange Commission (SEC) voted to approve orders allowing in-kind creations and redemptions for crypto asset exchange-traded products (ETPs), including those based on bitcoin and ether. This marks a significant shift from the SEC’s earlier stance, which had limited spot crypto ETPs to cash-only transactions.

Under the newly approved framework, authorized participants can now exchange crypto assets directly for ETP shares, bypassing the need to convert to U.S. dollars. This change aligns crypto ETPs with standard practices for commodity-based ETPs and was approved with an aim to reduce transaction costs, minimize price slippage, and improve overall market efficiency.

SEC Chairman Paul S. Atkins described the move as part of a broader effort to develop a “fit-for-purpose regulatory framework” for crypto markets. “Investors will benefit from these approvals, as they will make these products less costly and more efficient,” Atkins said in a statement. Commissioner Mark Uyeda echoed this sentiment, noting that the prior cash-only model imposed unnecessary burdens and created market asymmetries.

The SEC also approved several related measures, including:

ETPs holding mixed spot bitcoin and ether;

Options on certain spot bitcoin ETPs;

FLEX options on shares of certain BTC-based ETPs;

Increased position limits for listed options on BTC-based ETPs (up to 250,000 contracts); and

Scheduling orders seeking public comment on proposals to list and trade two large-cap crypto-based ETPs.

The SEC’s decision is expected to facilitate greater institutional participation by streamlining arbitrage and hedging strategies. While the move signals a more open regulatory posture under Chairman Atkins, stakeholders should remain attentive to how these changes are implemented and monitored. As the crypto ETP landscape continues to evolve, regulatory clarity will be key to fostering innovation while protecting investors.

UK Ancillary Activities Exemption Proposals Published for Commodity Derivatives and Emission Allowances

The Financial Conduct Authority (FCA) recently published a consultation (Consultation) setting out its proposed approach to revising the ancillary activities test (AAT), which forms part of the ancillary activities exemption (AAE) from investment firm authorisation under Markets in Financial Instruments Directive. Separately, HM Treasury (HMT) has published a near-final statutory instrument (SI) that will amend the Financial Services and Markets Act 2000 (Regulated Activities) Order 2001 (RAO) and confer rule-making powers on the FCA in respect of the AAE.

Background

The AAE allows a firm to be exempt from authorisation as an investment firm when its trading in commodity derivatives, emission allowances or derivatives of emission allowances satisfies the requirements of the AAT and provided the firm does not execute client orders, use a high frequency algorithmic trading technique or act as a market maker. Non-financial firms (i.e., end-users) can use the AAE to deal in commodity derivatives, emission allowances and related instruments, where such activity is ancillary to their main business, without becoming fully authorised investment firms.

Historically, to determine AAE eligibility, firms were required to perform a complex assessment, consisting of two main quantitative components: (a) the market share test, and (b) the main business test. Following Brexit, the European Securities and Markets Authority abolished the market share test and ceased publishing the related underlying market-wide data for the European Economic Area (EEA). The UK market share test, however, requires the market data of both the UK and the EEA. The FCA, therefore, issued a series of temporary statements to clarify that firms could continue to benefit from the AAE in the United Kingdom pursuant to Article 72J of the RAO.

Even when the EEA market share test data was available, however, the methodology required multiple asset-class calculations, sweeping in both cash- and physically-settled contracts and generating results that could swing materially with market volatility. Industry feedback requested a simpler, “de-minimis” style approach to the AAT in the UK similar to what has been adopted in the EU, US and Switzerland. As part of the UK’s Wholesale Markets Review, HMT committed to revoking the existing AAT and replacing it with a new, simplified version.

Key Proposals

The main proposals in the Consultation and amendments in the SI comprise:

amending the AAT by introducing three separate and independent tests to assess whether a firm can use the AAE. A non-financial firm may qualify for the AAE if it meets one of these tests each year:

the new annual threshold test (or “de-minimis” test), which will exempt a firm that undertakes trading in commodity derivatives on a relatively small scale. The FCA seeks views on the exact thresholds, with the two options being setting the threshold at (i) GBP 3 billion excluding certain transactions with or through UK-authorised firms, or (ii) GBP 5 billion including all cash-settled positions in derivatives traded on a UK trading venue. This would replace the current market share test;

the existing trading test, which is currently part of the main business test, with some modifications; or

the existing capital employed test, which is also part of the main business test, for which the FCA is also proposing some modifications; and

providing the FCA with a flexible rule-making power to define the necessary thresholds, detail calculation formulas, and adjust these measures as market conditions and policy objectives evolve.

Next Steps

Responses to the Consultation and the SI are due by 28 August 2025. Subject to parliamentary time, HMT expects to lay the SI before Parliament in autumn 2025. The FCA intends to publish its final policy statement in the last quarter of 2025 or the first quarter of 2026.

While the new regime will come into force on 1 January 2027, transitional relief under Article 72J of the RAO will continue to be available until 1 January 2028. This is intended to provide firms that are unable to rely on the new regime with time to obtain authorisation.

The Consultation, SI and HMT’s policy note are available here, here and here, respectively.

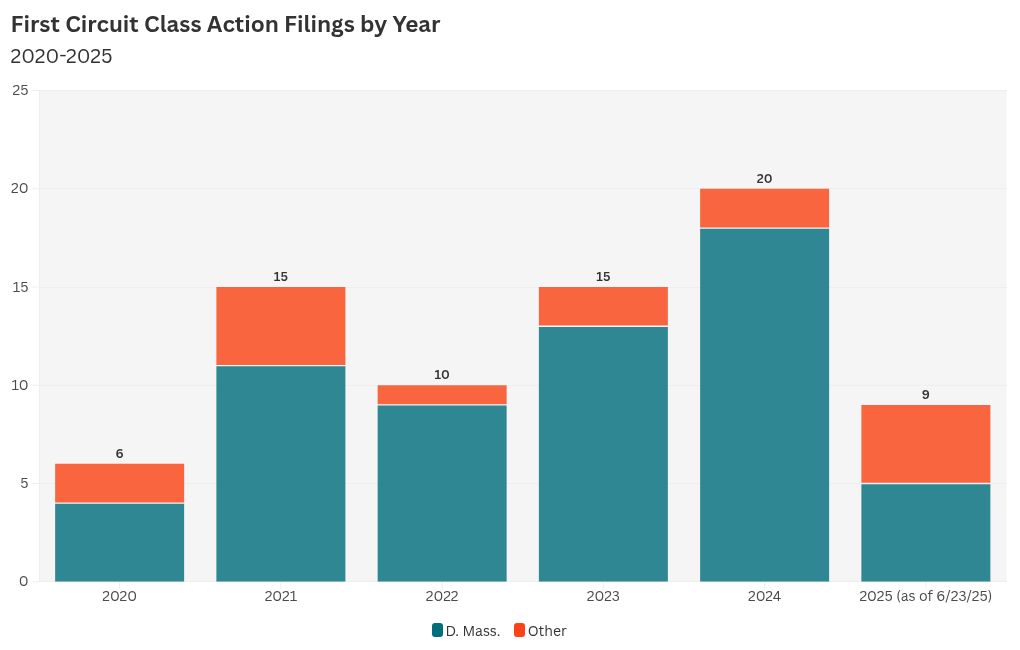

District of Massachusetts Sees Rise in Securities Fraud Class Actions Despite Dismissal Risks

This is part one of a three-part series exploring the recent uptick in securities class action filings in the First Circuit and examining recent decisions issued by the District of Massachusetts. This post examines current trends in securities class action filings and recent decisions on motions to dismiss in the District of Massachusetts.

Securities Class Action Trends in the First Circuit and District of Massachusetts

Securities fraud class action filings have surged within the First Circuit over the past five years. The rate of filings has more than doubled in a five-year period. In 2020, there were only six filings. By 2024, that number had climbed to twenty. As of June 2025, nine securities class actions have already been filed—on pace to exceed last year’s total. The vast majority of securities class action filings within the First Circuit have been in the District of Massachusetts, with twenty-three of the twenty-nine filings in the past eighteen months.

Within the First Circuit, plaintiffs are mainly bringing claims for securities fraud under Section 10(b) of the Securities Exchange Act of 1934 and Securities and Exchange Commission Rule 10b-5. To bring a Section 10(b) claim, plaintiffs must allege six key elements. These elements include: (1) a material misrepresentation or omission, (2) scienter, (3) a connection with the purchase or sale of a security, (4) reliance, (5) economic loss, and (6) loss causation. These allegations must meet the heightened pleading standards imposed by Federal Rule of Civil Procedure 9(b), as well as the Private Securities Litigation Reform Act (“PSLRA”).

Dismissal Rates in Securities Fraud Class Actions: District of Massachusetts Remains a Decisive and Rigorous Jurisdiction

Despite the rise in securities class action filings in the District of Massachusetts, they face intense scrutiny from the court at the pleading stage. Over the past five years, the court has granted motions to dismiss these claims at a higher rate than the national average, with 58% of motions to dismiss securities class actions granted in the District of Massachusetts (compared with 49.6% across all federal district courts). Further, the District of Massachusetts is more likely than other federal district courts to take an “all or nothing approach,” with only 8% of motions to dismiss receiving split decisions (compared with a 24.2% split decision rate across all federal district courts).

Recent opinions on motions to dismiss securities class actions by the District of Massachusetts have given particular scrutiny to the elements of material misrepresentation and scienter. The court’s analyses of these elements provide guidance for litigants bringing and defending securities fraud claims at historically high rates.

Part two of this three-part series will examine the District of Massachusetts’ approach to analyzing the material misrepresentation element in recent securities fraud class action cases.

* * *

Thank you to firm summer associate Jeff Supple for his contribution to this series.

Regulatory Update and Recent SEC Actions July 2025

Recent SEC Administration Changes

SEC Names Brian Daly as Director of the Division of Investment Management

On June 10, 2025, the Securities and Exchange Commission (the “SEC”) announced that Natasha Vij Greiner, Director of the Division of Investment Management, would leave the SEC effective July 4, 2025. Ms. Greiner had served in the role since March 2024. The SEC announced, on June 13, 2025, that Brian T. Daly would become the new Director of the Division of Investment Management, effective July 8, 2025. For the last four years, Mr. Daly has been a partner in the investment management practice of a law firm. Prior to that, he was a partner in the investment management group of a different law firm and served as general counsel and chief compliance officer in-house at multiple investment management companies. Mr. Daly earned his J.D. from Stanford Law School, his B.A. from Catholic University, and his M.A. from the East-West Center at the University of Hawaii

SEC Names Jamie Selway as Director of the Division of Trading and Markets

On June 18, 2025, the SEC announced that David Saltiel, the Acting Director of the Division of Trading and Markets, would leave the SEC effective July 4, 2025. He had served as Acting Director since December 2024 and had also served in this position previously in 2021. Following an SEC announcement on June 13, 2025, Jamie Selway took over as the Director of the Division of Trading and Markets, effective June 17, 2025. Prior to joining the SEC, Mr. Selway was a partner in private practice advising his clients on capital markets issues and served as a board member and advisor to multiple financial technology companies. Mr. Selway received his M.S. in financial mathematics from the University of Chicago and a B.A. in mathematics and European history from Washington & Lee University.

Other Changes in SEC Personnel

In addition to the changes in the two director positions, the SEC has made the following changes to key personnel:

Natalie Diez Riggin was named the Senior Adviser and Director of Legislative and Intergovernmental Affairs;

Kurt Hohl was named Chief Accountant;

Erik Hotmire will be returning to the SEC as the Chief External Affairs Officer and the Director of the Officer of Public Affairs; and

Kevin Muhlendorf was appointed the SEC’s Inspector General.

SEC Rulemaking

SEC Extends Effective and Compliance Dates for Amendments to Form N-PORT Reporting Requirements

The SEC announced on April 16, 2025, that it would be extending the effective and compliance dates for the amendments pertaining to Form N-PORT reporting requirements. As of April 22, 2025, the effective date for the amendments to Form N-PORT and amendatory instruction 2 to the rule under the Investment Company Act of 1940 Act, as amended (the “1940 Act”) associated with N-PORT reporting requirements (Rule 30b1-9) are delayed to November 17, 2027. The effective date for the amendatory instruction 3 to Rule 30b1-9 is delayed until May 18, 2028. The announcement extends the compliance date for fund groups with net assets of $1 billion as of their most recent fiscal year from November 17, 2025, to November 17, 2027. The compliance date for fund groups with less than $1 billion in net assets is extended from May 18, 2026, to May 18, 2028. The effective and compliances date for the amendments to Form N-CEN remain November 17, 2025. For a full discussion of the rule amendments, please see SEC Adopts Reporting Enhancements for Registered Investment Companies and Provides Guidance on Open-End Fund Liquidity Risk Management Programs, in our regulatory update here.

SEC Solicits Public Comment on the Foreign Private Issuer Definition

The SEC, on June 4, 2025, issued a concept release soliciting public comment on the definition of foreign private issuer. Foreign private issuers benefit from certain accommodations and exemptions from the disclosure and filing requirements of the federal securities laws. The concept release solicits public input on whether the changes in the population of foreign private issuers since 2003 warrant changes to the definition of foreign private issuer. The public comment period will remain open for ninety days following publication in the Federal Register.

Extension of Form PF Amendments Compliance Date

The SEC announced on June 11, 2025, that the SEC, along with the U.S. Commodity Futures Trading Commission, voted to further extend the compliance date for the amendments to Form PF until October 1, 2025. The amendments to Form PF, which were adopted on February 8, 2024, originally had a compliance date of March 12, 2025, which had previously been extended until June 12, 2025. For a full discussion of the rule amendments, please see SEC Adopts Rule Amendments to Enhance Private Fund Reporting, in our regulatory update here.

Extension of Compliance Date for Amendments to the Broker-Dealer Customer Protection Rule

The SEC announced on June 25, 2025, that it voted to extend the compliance date to June 30, 2026, for recently adopted amendments to Rule 15c3-3 under the Securities Exchange Act of 1934, as amended (known as the broker-dealer customer protection rule). The amendments, which were adopted by the SEC on December 20, 2024, originally had a compliance date of December 31, 2025. For a full discussion of the rule amendments, please see SEC Adopts

Rule Amendments to Broker-Dealer Customer Protection Rule, in our regulatory update here.

U.S. House of Representatives Reintroduces Bill to Increase Ability of Closed-End Funds to Invest in Private Funds

Representatives Ann Wagner and Gregory Meeks cosponsored a house bill, referred to as “The Increase Investor Opportunities Act” (the “Bill”), that would allow closed-end funds to invest more freely in private funds, which proponents of the Bill view as increasing the opportunity for retail investors to access private markets. The Bill would also limit the portion of closed-end fund shares that activist investors and their affiliates could acquire to no more than 10 percent.

SEC Formally Withdraws Fourteen Rule Proposals

On June 12, 2025, the SEC formally withdrew fourteen outstanding rule proposals issued by the prior administration. The SEC’s action highlights that any future rulemaking on the various topics will start with a new proposal and another chance for public comment. Below is a list of the withdrawn proposals:

Conflicts of Interest Associated with the Use of Predictive Data Analytics by Broker Dealers and Investment Advisers

Safeguarding Advisory Client Assets

Cybersecurity Risk Management Rule for Broker Dealers, Exchanges, and Other Market Infrastructure Entities

Regulation Best Execution

Order Competition Rule

Outsourcing by Investment Advisers

Enhanced Disclosures by Certain Investment Advisers andInvestment Companies About Environmental, Social and Governance Investment Practices

Cybersecurity Risk Management for Investment Advisers, Registered Investment Companies, and Business Development Companies

Volume Based Exchange Transaction Pricing for NMS Stocks

Position Reporting of Large Security Based Swap Positions

Regulation Systems Compliance and Integrity

Substantial Implementation, Duplication, and Resubmission of Shareholder Proposals Under Exchange Act Rule 14a-8

Amendments Regarding the Definition of “Exchange” and Alternative Trading Systems

Amendments to the National Market System Plan Governing the Consolidated Audit Trail to Enhance Data Security

SEC Enforcement Actions and Other Cases

SEC Charges Crypto Asset and Foreign Exchange Trading Company Founder with $198 Million Crypto Asset and Foreign Exchange Fraud Scheme

The SEC charged the founder (the “Founder” or “Defendant”) of a now-defunct entity that claimed to be a crypto asset and foreign exchange trading company (the “Company”) with the offering and selling of unregistered securities and violating antifraud provisions of securities laws. According to the SEC’s complaint, the Defendant, through the Company, sold “membership” packages that guaranteed investors high returns and offered members a multi-level-marketing- like referral incentive. Through the Company, the Founder raised approximately $198 million and spent more than $57 million on luxury items and personal expenses and used the remaining money to pay other investors their purported returns and referral rewards. In addition to the SEC’s charges, the Founder is facing criminal charges for the Ponzi-like scheme.

“[The Defendant] used the guise of innovation to lure investors into lining his pockets with millions of dollars while leaving many victims empty-handed,” said Laura D’Allaird, Chief of the Commission’s new Cyber and Emerging Technologies Unit. “In reality, his false claims of crypto industry expertise and a supposed AI-powered auto-trading platform were just masking an international securities fraud.”

SEC Charges Three Texans with Defrauding Investors in $91 Million Ponzi Scheme

The SEC, on April 29, 2025, announced charges against three individuals (each a “Defendant” and collectively, the “Defendants”) for operating a Ponzi scheme that raised at least $91 million from more than 200 investors. According to the SEC’s complaint, between approximately May 2021 and February 2024, the Defendants operated the scheme through a trust controlled by a Defendant. The complaint alleges that the Defendants falsely represented that investors would receive 12 guaranteed monthly payments of between 3 percent and 6 percent per month, with the principal investment to be returned after 14 months. The SEC alleges that two Defendants held the trust out as a highly profitable international bond trading business with billions in assets and told investors that the monthly returns were generated from international bond trading and related activities. According to the complaint, the Defendants also offered investors the option to protect their investments from risk of loss through the purchase of a purported financial instrument they called a “pay order.” In reality, as the SEC alleges, the trust had no material source of revenue, the purported monthly returns were actually Ponzi payments, and the protection offered by the “pay orders” was illusory. The Defendants misappropriated millions in investor funds for personal use, according to the complaint.

Real Estate Holding Company and Top Executives Charged in Offering Fraud That Raised More than $100 Million

The SEC, on May 20, 2025, announced charges against a real estate and pre-IPO holding company (the “Company”) and its top executives (the “Executives”, and collectively, with the Company, the “Defendants”) for false and misleading statements in an offering of certificates that purportedly conveyed rights to receive crypto assets and an offering of the Company’s common stock. The SEC alleges that the Defendants broadly marketed the rights certificates to the general public and convinced more than 5,000 investors to purchase rights certificates through false and misleading statements including that the tokens underlying the rights certificates were backed by billions of dollars in real estate and equity interest in pre-IPO companies, when the Company’s assets were never worth more than a small fraction of that amount. The SEC’s complaint charges the Defendants with violations of the antifraud provisions of the federal securities laws.

SEC Charges Former Real Estate Investment CEO with Operating Multimillion Dollar Ponzi-Like Scheme

The SEC announced charges against the former CEO (the “Former CEO”) of a real estate investment business, with defrauding approximately 200 investors of at least $46 million by selling them fake interests in real estate investment limited partnerships. According to the SEC’s complaint, the Former CEO managed legitimate limited partnerships that invested in residential and commercial real estate, and that were owned by a set of real investors. From approximately 2007 to April 2024, the Former CEO allegedly offered and sold fake ownership interests in these limited partnerships to defrauded investors. According to the complaint, the fake sales were not reflected in the legitimate records of ownership, and investors who purchased the fake interests never became actual limited partners or received ownership rights. Instead, the Former CEO allegedly commingled new investor funds with personal and business funds and used the commingled funds to make Ponzi-like payments, gave defrauded investors false tax records, and misappropriated investor funds to pay for personal expenses and real estate transactions and expenses related to his personal partnership. The SEC’s complaint charges the Former CEO with violating the antifraud and registration provisions of the federal securities laws.

SEC Drops Liquidity Rule Case, Including Charges Against Two Former Directors