Rule 506(c) Unchained? The SEC Loosens Requirements for Advertising in Private Capital Raises

On 12 March 2025, the US Securities and Exchange Commission (SEC) staff issued a no-action letter that provides private fund sponsors with a concrete, streamlined approach to relying on Rule 506(c),1 based on minimum investment amounts and investor representations. This guidance has the potential to unlock Rule 506(c)’s advantages for private fund sponsors more than a decade after its passage.

Background on Rule 506(c)

Implemented in 2013 pursuant to the Jumpstart Our Business Startups Act, Rule 506(c) provides an alternative to the traditional prohibition on general solicitation in private offerings. Specifically, Rule 506(c) permits issuers to engage in general solicitation and advertising when selling securities, provided they take “reasonable steps” to verify that all purchasers are accredited investors. While enacted in order to give issuers the opportunity to increase their fundraising abilities through marketing to a public audience, Rule 506(c) has been only sparingly used over the last decade. This past November, SEC Commissioner Hester Peirce commented that issuers had “raised around $169 billion annually under Rule 506(c) compared to $2.7 trillion under 506(b), which does not permit general solicitation.”2

The “reasonable steps” verification requirement has presented operational challenges for many issuers. Prior methods qualifying as “reasonable steps” included reviewing tax returns, bank statements, or obtaining verification letters from professionals such as lawyers or accountants. Because of the additional administrative burdens imposed by these verification methods, Rule 506(c) has not been widely utilized, despite its potential to access a much wider audience for capital raising.

The Alternative Verification Method

The no-action letter provides a far less labor-intensive approach to satisfying Rule 506(c)’s verification requirements by streamlining the process issuers must follow to verify an investor’s accredited investor status. Specifically, the SEC mandates that an issuer relying on the no-action letter:

Impose minimum investment amounts of US$200,000 for individuals and US$1 million for legal entities;3

Receive written, self-certified representations from an investor that they are an accredited investor and that their investment is not financed by a third party for the specific purpose of making the particular investment;4 and

Have no actual knowledge of facts contrary to the two above bullets.

This test for determining whether an issuer has taken reasonable steps to verify accredited investor status is objective and depends on the specific facts and circumstances of each investor and transaction.

Practical Considerations for Private Fund Sponsors and Other Issuers

What are the practical implications for private fund sponsors now that the SEC has loosened the verification restrictions? Will private fund sponsors now jump into the fray and begin to advertise on social media, at sporting events, and elsewhere? There remain a number of considerations notwithstanding the less burdensome verification process. The SEC’s no-action letter addressed only this aspect of using Rule 506(c). The Marketing Rule (defined below), antifraud provisions, and other provisions of the Investment Advisers Act of 1940 the (Advisers Act) of course remain in full force and effect. Private fund sponsors considering an offering under Rule 506(c) will need to not only comply with the Advisers Act’s requirements, but be prepared to do so in front of a much wider investor and regulator audience.

Private fund sponsors considering Rule 506(c) offerings should note several additional considerations:

Update Policies and Procedures

Managers should adopt policies and procedures to accommodate Rule 506(c) offerings.

Marketing Rule

Registered investment advisers must continue to consider Rule 206(4)-15 under the Advisers Act the (Marketing Rule) when marketing their funds. While advisers may widely distribute marketing materials, such materials must comply with the Marketing Rule. For example, under the Marketing Rule, advisers are generally prohibited from including hypothetical performance, such as performance targets and projected returns, in advertisements to the general public.6

Switching Exemptions

Managers that want to change to a Rule 506(c) offering should file an updated Form D with the SEC and review offering materials for any necessary updates (e.g., remove representations regarding no general solicitation from subscription agreements and other documents).

What Is Next for Private Fund Sponsors and Rule 506(c)?

The easing of the investor verification process under Rule 506(c) will undoubtedly renew interest in pursuing this alternative path to capital raising. It is no secret that the fundraising environment over the last several years has been challenging, particularly for mid-market and emerging manager sponsors. For those managers, there are good reasons to explore general solicitation under Rule 506(c), bearing in mind the need to comply with the SEC’s recent guidance on verification and the requirements of the Advisers Act. Time will tell whether the SEC’s no-action letter will actually open the floodgates of advertising for private fund sponsors. Watch this space for further insights as the industry’s approach to using Rule 506(c) unfolds.

Footnotes

1 17 C.F.R. § 230.506(c) (1933).

2 https://www.sec.gov/newsroom/speeches-statements/peirce-remarks-sbcfac-111324

3 For an entity investor accredited solely through its beneficial owners, the minimum investment amount is US$1 million, or US$200,000 for each beneficial owner if the entity has fewer than five natural person owners.

4 These representations must be made for each beneficial owner for entities that are accredited solely through the accredited investor status of each beneficial owner.

5 17 C.F.R. § 275.206(4)-1 (●).

6 The Marketing Rule requires that investment advisers only present hypothetical performance to audiences if it is relevant to their likely financial situation and investment objectives, limiting an adviser’s ability to include such performance in advertisements to the public. In the Marketing Rule’s adopting release, the SEC specifically noted that advisers “generally would not be able to include hypothetical performance in advertisements directed to a mass audience or intended for general circulation.” Investment Adviser Marketing, Release No. IA-5653, SEC Dec. 22, 2020 effective May 4, 2021, at 220.

No APA Review of Commission Refusal to Issue Sua Sponte Show Cause Order

The US Court of Appeals for the Federal Circuit dismissed an appeal challenging a US International Trade Commission decision that upheld an administrative law judge’s (ALJ) order, ruling that such an order was within the Commission’s discretion and unreviewable. Realtek Semiconductor Corp. v. International Trade Commission, Case No. 23-1095 (Fed. Cir. Mar. 18, 2025) (Moore, C.J.; Reyna, Taranto, JJ.)

DivX filed a complaint at the Commission against Realtek alleging a violation of § 1337 of the Tarriff Act. DivX later withdrew the complaint. Realtek subsequently filed a motion for sanctions against DivX, alleging certain misconduct. The ALJ denied the motion on procedural grounds. Realtek subsequently petitioned for Commission review, asking the Commission to exercise its authority to issue a sua sponte order requiring DivX to show cause explaining why it had not engaged in sanctionable conduct. The Commission decided not to review and adopted the ALJ’s order without comment.

Realtek appealed, contending that the Commission violated the Administrative Procedure Act (APA) by not issuing a sua sponte show cause order. The Commission argued that Realtek’s appeal should be dismissed, contending that the issue raised was unreviewable.

The Federal Circuit agreed with the Commission, stating that under § 701(a)(2) of the APA, decisions made by an agency are unreviewable by the Court when they are entrusted to the agency’s discretion by law. The Court explained that the sua sponte issuance of a show cause order is a decision that “may be, not must be,” entered by the ALJ or on the Commission’s initiative. Therefore, the decision not to act sua sponte is a decision that remains wholly within the agency’s discretion.

The Federal Circuit rejected Realtek’s argument that the Commission’s refusal to act was reviewable because the Commission failed to provide reasoning, and that Commission review would have allowed the Court to determine if there were “illegal shenanigans” in exercising discretion. However, the case cited by Realtek involved the review of “shenanigans” that fell within the Court’s reviewable categories, not one related to the Commission’s refusal to issue a show cause order sua sponte. The Court found no support for Realtek’s claim that discretionary agency actions under § 701(a)(2) become reviewable under the APA simply because the agency fails to provide its reasoning.

GeTtin’ SALTy Episode 49 | Conformity—Policy or Politics? [Podcast]

In this episode of GeTtin’ SALTy, host Nikki Dobay dives into the complex and timely topic of tax conformity with two state tax guests, Shail Shah, Greenberg Traurig shareholder based in San Francisco, and Jeff Newgard, President and CEO of Peak Policy. The discussion centers on the challenges and implications of how states align—or don’t align—with the federal Internal Revenue Code (IRC).

Key topics include:

Oregon’s Proposed Shift to Static Conformity

California’s Static Conformity Challenges

Administrative and Compliance Impacts

Broader Implications for Tax Policy

Future Outlook

In a lighthearted conclusion, Nikki, Shail, and Jeff reveal which Muppet or Sesame Street character best represents their tax policy personas!

This episode is a must-listen for anyone navigating the intricacies of state and local tax policy, offering a deep dive into conformity issues and their broader implications for taxpayers and state governments alike.

New Office of Financial Sanctions Implementation Financial Services Threat Assessment

On 13 February 2025, the Office of Financial Sanctions Implementation (OFSI) published its assessment of suspected sanctions breaches involving financial services firms since February 2022 (the Assessment). The Assessment forms part of a series of sector-specific assessments by OFSI that address threats to UK financial sanctions compliance by UK financial or credit institutions.

The Assessment highlights three areas of main concern:

Compliance;

Russian-Designated Persons (DPs) and enablers; and

Intermediary Countries.

This alert provides a summary of these concerns and suggests action financial services firms can take to combat these threats when developing their risk-based approach to compliance.

Compliance

OFSI has identified several compliance issues and advised steps that firms can take to improve and strengthen their compliance. These include:

Improper Maintenance of Frozen Assets

All DPs accounts and associated cards, including those held by entities owned or controlled by DPs, must be operated in accordance with asset freeze prohibitions and OFSI licence permissions. Financial institutions should review existing policies or contracts as these can often automatically renew, resulting in debits from DP accounts.

Breaches of Specific and General OFSI Licence Conditions

Firms need to carefully review permissions when assisting with transactions they believe are permitted under OFSI licences. Firms must ensure that OFSI licenses are in date, bank accounts are specified in OFSI licences and licence reporting requirements are adhered to.

Inaccurate Ownership Assessments

Firms must be able to identify entities that are directly owned by Russian DPs, and subsidiaries owned by Russian conglomerates that are themselves designated or majority owned by a Russian DP. Firms should conduct increased due diligence where necessary and regularly update due diligence software.

Inaccurate UK Nexus Assessments

Firms should take extra care to understand the involvement of UK nationals or entities in transaction chains when assessing the application of a UK nexus. They must also ensure they understand the difference between United Kingdom, European Union and United States sanctions regimes to make correct assessments of how UK sanctions might be engaged.

Russian DPs and Enablers

OFSI defines an enabler as “any individual or entity providing services or assistance on behalf of or for the benefit of DPs to breach UK financial sanctions prohibitions.” Broadly, there are two types of enablers:

professional enablers that provide professional services “that enable criminality. Their behaviour is deliberate, reckless, improper, dishonest and/or negligent through a failure to meet their professional and regulatory obligations”; and

non-professional enablers, such as family members, ex-spouses or associates.

Maintaining Lifestyles and Assets

Most identified enabler activity has been in relation to maintaining the lifestyles of Russian DPs and assets as they face growing liquidity pressures from UK sanctions.

OFSI urges firms to scrutinise the following red flags:

New individuals or entities making payments to satisfy obligations formerly met by a DP;

Individuals connected to Russian DPs receiving funds of substantial value;

Regular payments between companies owned or controlled by a DP;

Crypto-asset to fiat transactions involving close associates of a Russian DP;

Family member of a DP that is an additional cardholder on a purchasing card that uses the card for personal expenses and overseas travel; and

Deposits of large sums of cash without sufficient explanation;

Fronting

With a significant value of the assets of DPs having been frozen in the United Kingdom, an increasing amount of enablers are attempting to front on behalf of DPs and claim ownership of frozen assets. The links between enablers fronting on behalf of DPs are not always clear, and so OFSI has outlined several red flags for firms to be aware of:

Individuals with limited profiles in the public domain, for instance, those with limited related professional experience;

Inconsistent name spellings or transliterations;

Recently obtained non-Russian citizenships; and

Repeated or unexplained name changes or declared location of operation.

Utilising Alternative Payment Methods to Breach Prohibitions

Financial services firms need to remain diligent when assessing the threat posed by the increasingly sophisticated methods employed by DPs and enablers to evade UK financial sanctions prohibitions. Particular attention should be paid to attempts at money laundering on behalf of Russian DPs, including any indications of high value crypto-asset to cash transfers.

Intermediary Countries

Emphasis is placed on the use of intermediary jurisdictions in suspected breaches of UK financial sanctions prohibitions. The following jurisdictions are utilised most often: British Virgin Islands, Guernsey, Cyprus, Switzerland, Austria, Luxembourg, United Arab Emirates and Turkey. These jurisdictions offer secrecy or particular commercial interests.

There has also been a change in the third countries referenced in suspected breach reports, with increased activity in the Isle of Man, Guernsey, United Arab Emirates and Turkey. Indeed, the United Arab Emirates accounted for the largest section of suspected breaches reported to OFSI in the first quarter of 2024. This shift has likely been caused by various factors, including capital flight by Russians to jurisdictions that do not have sanctions on Russia.

The Assessment helpfully outlines a non-exhaustive list of specific activities in various countries that could be indicative of UK financial sanctions breaches. Financial institutions are encouraged to review and familiarise themselves with this list so that they can identify potential threats to sanctions compliance. Businesses should then consider the involvement of these jurisdictions when conducting due diligence, and evaluate the risks associated with various transactions.

Conclusion

The recent expansion of the United Kingdom’s financial sanctions regime, particularly in relation to Russia’s invasion of Ukraine, has resulted in sanctions evasion becoming increasingly sophisticated and widespread. Considering the scale of evasion being conducted, financial institutions need to remain proactive and vigilant in identifying transaction activity that may be indicative of attempts to circumvent UK sanctions regimes.

When designing sanctions compliance programmes, financial institutions should refer to the Assessment to account for methodologies of evasion and recognise specific behaviours that might present warning signs. By taking a proactive approach to prevent their services from being exploited as instruments of circumvention, financial institutions will contribute to efforts to combat sanctions evasion, whilst avoiding the financial and reputational repercussions of non-compliance.

If you have any questions on the Assessment or want further advice on developing your policies for UK sanctions compliance, please do not hesitate to contact our Policy and Regulatory practice.

Louisiana Industrial Tax Exemption Program (ITEP) – New Rules and Executive Order

On March 20, 2025, Governor Landry issued Executive Order No. JML 25-033 and Louisiana Economic Development (LED)/Board of Commerce and Industry promulgated new rules (beginning at p. 366) which make changes to Louisiana’s Industrial Tax Exemption Program (ITEP).

The changes, in part, recognize Governor Landry’s view of the importance of the ITEP as an economic development tool to encourage capital investment in Louisiana manufacturing projects. Among other changes, businesses with existing ITEP contracts under the 2017 and 2018 ITEP Rules may “opt out” of the jobs, payroll, and compliance components regardless of whether the contract is up for renewal.

Businesses with existing ITEP contracts under the old rules may want to consider opting out of the jobs, payroll, and compliance components of those contracts. The “Opt-Out” Amendment Form may be filed via LED’s Fastlane NextGen.

Among other changes, businesses with existing ITEP contracts under the 2017 and 2018 ITEP Rules may “opt out” of the jobs, payroll, and compliance components regardless of whether the contract is up for renewal.

Keep California Rolling: New Bills Poised to Revitalize Production (in Hollywood)

The introduction of Senate Bill 630 and Assembly Bill 1138 aims to provide California with a competitive advantage in its quest to retain and bring back production jobs that are vital to the entertainment industry. The bills were introduced by Senator Ben Allen, Assembly Members, Rick Chavez Zbur, and Isaac Bryan, with a focus on job creation and promise to diversify the types of productions that qualify for California’s Film and Television Tax Credit program. SB 630 and AB 1138 will be referred to respective policy committees over the coming weeks. Governor Gavin Newsom has also unveiled plans to more than double California’s current tax credit cap to provide much-needed relief for the entertainment industry following COVID-19 shutdowns, the strikes, LA wildfires and mass exodus of film and television production from California.

SB 630 and AB 1138 are intended to amend, update, and modernize California’s Film and Television Tax Credit Program, with the stated goal of protecting and bringing back jobs that have left, and continue to leave California for other more lucrative production locations, and to ensure that California remains competitive in the industry. SB 630 and AB 1138 would increase the rebate by an unspecified amount from the 20% that is currently offered to most productions in California. Each law would also expand types of productions that are eligible for the tax incentives, by including animation, game shows, and other unscripted programming, each of which is currently excluded.

In an effort to bolster this momentum, the Entertainment Union Coalition has launched a campaign called “Keep California Rolling”, which aims to keep film and television jobs in California.” The initiative is labor-led and its main purpose is to emphasize the importance of exploring new ways to attract film and television production back to the state, as well as support Governor Newsom’s proposal to expand the California Film & TV Tax Credit from $330 million annually to $750 million. However, though likely to be approved, this expansion hinges on California’s 2025-2026 budget which is currently being negotiated.

Several member entities of the Entertainment Union Coalition have traveled to Sacramento to lobby lawmakers in support of this jobs-based program, including the Directors Guild of America, LiUNA! Local 724, SAG-AFTRA, Teamsters Local 399, Writers Guild of America West, California IATSE Council, and the American Federation of Musicians. Collectively, the Entertainment Union Coalition represents over 165,000 members who live and work in California’s entertainment industry. If Governor Newsom’s proposal passes, it will prove to be the most significant expansion to the program in decades.

Production jobs being lured away to different territories has been an issue plaguing California for decades, as the financial incentives in other states and countries have proven too lucrative to pass up–Georgia, Ontario and the United Kingdom have no caps on their subsidies for film and television productions. According to recent reports from FilmLA and the Entertainment Union Coalition, production in Los Angeles was down 30% over five-year averages in 2024 and approximately 50% of the 312 productions did not qualify for California’s tax credit incentive from 2015 to 2020. SB 630 and AB 1138 aim to change that trajectory and create a sustainable environment that keeps jobs and economic benefits in California.

Jennifer Hays contributed to this article.

Australian Federal Budget 2025-2026–Key Tax Measures and Instant Insights

The Australian Federal Government has just released its budget for 2025-26. The K&L Gates tax team outlines the key announced tax measures and our instant insights into what they mean for you in practice.

In summary, with an upcoming Australian federal election, the budget is light on substantive tax changes (other than personal income tax cuts), and largely defers measures to raise further revenue or amend the tax system until after the election. Whilst there will be some relief that there have not been further targeted tax measures (e.g. on multinationals), there is also likely to be disappointment that there has been no attempt at tax reform or addressing the large number of outstanding matters requiring clarification.

Key Announced Tax Measure

K&L Gates Instant Insights

Personal Income Tax Cuts From 1 July 2026

The Government has announced reductions in the first tax rate from 16% to 15% from 1 July 2026 and from 15% to 14% from 1 July 2027.

The Government has also increased the income threshold for where the 2% Medicare levy applies.

These will no doubt be welcome for individuals, and will likely form a key part of the Government’s campaign for re-election.

These changes have been largely targeted at low to middle income earners, although the tax cuts will apply to all taxpayers. Given the higher rates of inflation and wage growth, this essentially returns some (but not all) of the higher income tax take from “bracket creep” to taxpayers.

There is no relief however for businesses, small or large.

Managed Investment Trust (MIT) “Clarifications”

The Government is proposing to legislate to allow foreign widely held pension funds and sovereign funds to get access to the reduced MIT withholding tax rates on eligible income for “captive” MITs (i.e. where they are the sole actual or beneficial member of the MIT).

This is intended to “complement” the Australian Taxation Office’s (ATO’s) Taxpayer Alert TA 2025 / 1 which focused on restructuring to access MIT benefits and using structures to implement captive MITs.

This is a pre-announced, welcome change that confirms existing industry practice, and addresses a difference between the rules to qualify as a MIT and the rules to apply reduced withholding tax.

However, it was only necessary due to the ripple of serious concerns started by TA 2025/1 and focusing on “captive MITs” without sufficient clarity on the ATO’s concerns.

It remains clear that the ATO has a focus on foreign collective investment vehicles (i.e. funds) accessing MIT withholding concessions where they are the sole ultimate owner (even though they may themselves by widely held).

No Changes to Address Taxation of “Digital” Assets–Handball to the ATO

The Government has confirmed it will not legislate any amendments to the taxation laws to deal with the array of digital assets, such as “decentralised finance” (DeFi), gaming finance (GameFi) and non-fungible tokens (NFTs).

It also (in a fairly luke-warm way) endorsed the principles developed by the Board of Taxation (BoT) to guide taxation of digital assets, whilst also indicating that further ATO guidance will be available to address uncertainty.

Whilst the lack of a specific tax regime for digital assets is consistent with the BoT’s recommendations, the tepid endorsement of the BoT’s policy framework for digital assets provides little guidance on how the ATO is to develop further tax guidance to address the taxation of these novel assets, leaving the ATO to largely continue to act as policy formulator and implementor as well as revenue collector.

Based on the existing guidance, it is unlikely this will result in much relief for digital asset providers, platforms or investors.

No Further Guidance on Corporate Tax Residency

The Government has provided no update on the changes (promised back in Federal Budget 2020/21) on clarifying corporate residency laws, particularly following hardening of ATO guidance on corporate residency.

This means the ATO’s views in TR 2018/5 and PCG 2018/9 continue to be applied (notwithstanding the Government’s previously stated intent to address some of the challenges associated with those rules).

Foreign entities with Australian directors etc continue to face heightened risks of the ATO trying to allege Australian tax residency.

Announced but Unenacted Measures

The budget largely provides no clarity on a number of previously announced but unenacted measures, including:

Changes to increase scope of foreign resident CGT withholding tax – other than that this has been delayed until after legislation is enacted;

Clean building MIT rates for data centres and warehouses has been delayed until after legislation is enacted;

Small business instant asset write-off extension to 30 June 2025;

Part IVA amendments to deal with withholding tax;

CGT rollovers and response to the BoT’s review;

Additional taxation of superannuation balances over AU$3 million, including whether this incorporates unrealised gains; and

Changes to Division 7A (i.e. removal of distributable surplus requirement).

The list of announced but unenacted tax measures continues to grow and provides real uncertainty for the tax system and all taxpayers. Whilst there are some positive amendments, including deferring the commencement of the unreleased changes to foreign resident capital gains withholding, it largely leaves these matters unresolved.

Some of the measures, such as taxation of superannuation balances, are clearly baked into the budget revenue forecasts, and so although the Government has not succeeded in getting legislation passed, the intent remains to do so (pending its re-election).

The Government also appears to be in wait and see mode as to what the ultimate outcome is in the Bendel litigation to determine next steps on Division 7A.

However, there has been little or no clarity provided on most measures, and so taxpayers continue to face uncertainty. Whether we see some measures proceed will ultimately depend on the outcome of the election.

Continued Focus on Tax Integrity by the ATO

The Government has provided further funding to the ATO to address tax integrity and target tax avoidance arrangements, particularly focused on multinationals.

The Government has also provided additional funding to the ATO to address non-payment of superannuation contributions and amounts PAYG withheld on account of tax.

This will see the ATO continue to target key concerns – based on our experiences, in recent years this has involved multinationals, foreign investors (including private equity funds) and intellectual property arrangements.

The continued focus on entities using the PAYG withholding and superannuation contribution regimes as a source of funding is unsurprising, and we have seen dramatically increased ATO activity in this space. This has led to increased insolvencies in small to medium businesses.

Understanding Partial Redemptions for Startup Founders

Being a startup founder is hard. Among other things, startup founders face long hours, resource constraints, intense pressure, and the need for constant adaptation and resilience in the face of uncertainty. Founders face all these tasks while also being severely underpaid, adding to the list of trials one of the more challenging: personal financial pressure.

As a result of such financial pressure, and the frightening uncertainty of success, it is not unusual for founders to consider a partial redemption or liquidity event in which they sell a portion of their shares to the company or directly to an investor, typically as part of a proposed financing round. Such a redemption provides cash to the founder in exchange for a reduced level of ownership and risk in the company. A partial redemption may be accomplished through a cash purchase directly from the company or by using a portion of the proceeds from a financing round. A partial redemption can be a strategic move with both advantages and potential drawbacks. Understanding the nuances of this transaction is crucial for founders and investors alike.

Why Consider Partial Redemption?

Several factors might drive a company to pursue a partial redemption of the founder’s shares:

Liquidity: Founders may seek to cash out a portion of their equity for personal or financial reasons.

Tax Planning: Partial redemption can offer tax advantages, especially when structured carefully.

Corporate Governance: Reducing the concentration of ownership can improve corporate governance and decision-making.

Employee Incentive Plans: Repurchased shares can be used to fund employee stock option plans or other incentive programs.

Key Considerations:

Before embarking on a partial redemption, several factors must be carefully evaluated:

Valuation: Accurately valuing the company’s shares is essential for determining a fair redemption price. The company should review the current 409A valuation and consider the potential impact the partial redemption will have on future 409A valuations.

Tax Implications: The tax consequences for both the company and the founder can vary significantly based on factors such as the founder’s holding period, the redemption structure and the company’s tax status. In general, a shareholder may exclude 100% of gain from the redemption of Qualified Small Business Stock (QSBS) for federal income tax purposes if certain issuance date and holding period requirements are met. However, a founder’s redemption may be disqualified from QSBS tax treatment.

Corporate Structure: The company’s legal structure and governing documents may impose limitations or restrictions on share redemptions.

Financial Impact: Repurchasing shares can reduce the company’s cash reserves and potentially affect its financial performance.

Shareholder Agreement/Investment Documents: Existing shareholder agreements or investment documents may contain provisions related to share transfers, redemptions, rights of first refusal, right of co-sale or tag-along rights. The partial redemption may trigger rights for existing shareholders who may wish to participate in the sale.

Potential Drawbacks:

While partial redemption can offer benefits, it also carries potential risks:

Dilution of Ownership: If the redemption is not carefully structured, it can lead to dilution of ownership for existing shareholders.

Company’s QSBS: Impact on Qualified Small Business Stock (QSBS) for existing shares as well as future purchases.

Market Perception: A significant share repurchase can sometimes be interpreted negatively by the market.

Loss of Talent: Founders may feel less motivated or committed to the company after a partial redemption.

The decision to redeem a founder’s shares is complex. Early exits and partial redemptions can provide liquidity and diversification for founders while allowing them to maintain some ownership in the company. However, it is important to consider the potential risks, structuring options and tax implications before the company and founder engage in such a redemption.

Essential Tax and Compliance Insights for Private Medical Practices in 2025

As we move into 2025, the healthcare sector continues to experience significant changes in tax and compliance regulations, especially for private medical practices and NHS contractors. Whether you’re running a private clinic or working as an NHS contractor, staying up-to-date with the latest tax laws and financial obligations is crucial for the success and sustainability […]

CMS’s ACA Marketplace Integrity and Affordability Proposed Rule – What it may mean for Health Plans

Earlier this month, the Centers for Medicare & Medicaid Services (CMS) released its 2025 Marketplace Integrity and Affordability Proposed Rule (Proposed Rule), proposing a number of enrollment and eligibility policies impacting both Federal and State Exchanges. While CMS frames these policies as necessary to combat fraud and abuse, the impact will be a reduction in enrollment in the ACA Marketplace – with the Proposed Rule estimating that between 750,000 and 2 million fewer individuals enroll in health insurance plans on the Exchanges in 2026.

The effective date of most of these provisions also coincides with the expiration of the enhanced premium subsidies, which the Biden administration extended through December 31, 2025 through the Inflation Reduction Act (IRA). These enhanced subsidiaries increased the amount of financial assistance individuals received and expanded eligibility for assistance. On December 5, 2024, the Congressional Budget Office wrote a letter to Congress indicating that the failure to extend these subsidies would result in 2.2 million individuals losing coverage in 2026 and an increase in premiums by 4.3%.

This article outlines the major provisions of the Proposed Rule, followed by a discussion of their potential impact on plans participating in the ACA Marketplace.

Key Provisions of the Proposed Rule

Income Verification Policies. In its Proposed Rule, CMS proposes several changes to the income verification process for applicants to apply through the Exchanges. Although CMS stated that these policies are necessary to combat fraud, CMS provided limited examples and evidence of fraud. Such policies include:

Removing the exception allowing Exchanges to rely on an applicant’s self-attestation of projected income, if the Internal Revenue Service (IRS) does not have tax return data to verify household income and family size. Exchanges would need to verify individuals’ enrollment, requiring enrollees to provide additional documentation.

Requiring additional income verification in instances where an applicant’s self-reported projected household income is between 100% and 400% of the Federal poverty level (FPL) but federal tax or other data shows that an applicant’s prior year’s income was below 100%. Individuals would have to prove that their income for the upcoming year is between 100% to 400% of the FPL or be unable to enroll in a plan on an Exchange. This change intends to attempt to identify individuals who may “overinflate” their income to be eligible for coverage. Currently, no income verification is required if the applicant projects a higher income than in their tax return.

Eliminating an automatic 60-day extension (in addition to the general 90-day deadline) when documentation is needed to verify household income in instances of income inconsistency.

Allowing Insurers to Deny Coverage for Past Due Premiums. CMS proposes to repeal a provision which currently prohibits insurers from requiring enrollees to pay past-due premium amounts in order to receive coverage under a new insurance policy or contract term. CMS consequently proposes, subject to state law, to allow insurers to add an enrollee’s past-due premium amount to the initial premium amount the enrollee must pay to effectuate coverage under a new policy or contract term and allow insurers to deny coverage to individuals if the total of past-due premiums and the initial premium amount are not paid in full. The stated purpose of this policy is (i) to curtail individuals from taking advantage of guaranteed coverage and seeking coverage when they need health care services, and (ii) to strengthen the risk pool and lower gross premiums.

Revision of Premium Payment Thresholds. CMS proposes to remove flexibilities that currently allow insurers to implement a fixed dollar and/or gross percentage-based premium payment threshold. Under current rules, insurers may consider enrollees to have fully paid their premiums if (i) under the fixed-dollar premium payment threshold, the enrollee has paid a total premium amount such that the unpaid remainder is $10 or less (adjusted for inflation), or (ii) under the gross percentage-based premium payment threshold, the enrollee has paid a total premium amount sufficient to achieve 98% or greater of the total gross monthly premium of the policy before the application of the advance premium tax credit (APTC). Under the Proposed Rule, insurers would only be allowed to implement a net premium percentage-based payment method where enrollees can meet the threshold by paying a total premium amount sufficient to achieve 95% or greater of the total net monthly premium amount owed.

Ineligibility for APTCs after one Year of Failing to Reconcile. CMS proposes to revise the “failure to file and reconcile process” by reinstating a 2015 policy that requires Exchanges to determine whether an individual is ineligible for the APTC if he or she did not file a Federal income tax return and reconcile their APTC amount in any given year. Currently, individuals will be deemed ineligible for failure to file and reconcile for a two-year span.

Changes to Open and Special Enrollment Periods. Under the Proposed Rule, CMS also seeks to shorten the Open Enrollment Period (OEP) and make several changes to Special Enrollment Periods (SEPs), including:

Shortening the OEP for all individual market Exchanges and off-Exchange individual health insurance (that are non-grandfathered) from November 1st to January 15th to November 1st to December 15th.

Removing the “low-income SEP” from both the Federal and State Exchanges. Currently, individuals whose projected household income is at or below 150% of the FPL have a SEP under the Federal and most State-based Exchanges whereby they can enroll or change plans on a monthly basis. CMS is proposing to remove this SEP. The stated purpose of this action is to reduce adverse selection (i.e., reduce the number of enrollees who sign up for health insurance only when they need coverage).

Requiring pre-enrollment verifications for applicants seeking coverage through a SEP. Currently, the Exchanges allow applicants to self-attest that, due to a change of circumstance, they qualify for a SEP (e.g., loss of employer coverage, marriage). The Proposed Rule would change the ability to self-attest and require applicants to submit documentation to the Exchanges.

Requiring Active Re-Enrollment. CMS also seeks to eliminate automatic re-enrollment for fully subsidized enrollees by proposing to require that enrollees whose premium payment amount would be $0 after application of the APTC, would be required to pay a $5 monthly premium until they update their Exchange application with an eligibility redetermination confirming their eligibility for the APTC.

Repeal of Bronze to Silver Plan Cross-Walking. CMS proposes to repeal regulations that currently allow Exchanges to move enrollees eligible for cost sharing reduction, which covers the cost of out-of-pocket healthcare costs and deductibles, from a bronze Qualified Health Plan (QHP) to a silver QHP for an upcoming plan year if a silver QHP is available (i) in the same product, (ii) with the same provider network, and (iii) with a lower or equivalent net premium post APTC-application.

Ineligibility of DACA Recipients. CMS proposes to remove Deferred Action for Childhood Arrivals (DACA) recipients from the definition of “lawfully present,” which in effect renders DACA recipients ineligible for enrollment in a QHP through the Exchange.

Prohibition of Coverage of Gender Affirming Care. CMS proposes to prohibit health insurance plans subject to the ACA’s essential health benefits (EHBs) from providing sex-trait modification, also commonly known as gender-affirming care, beginning Plan Year 2026. EHBs are ACA required minimum coverage categories that plans subject to the ACA must cover; EHBs are state or region specific and are determined based upon comparison to an EHB-benchmark plan that all other plans must mirror. This prohibition would in effect restrict all non-grandfathered insurance plans in the individual and small group markets, on- and off- Exchange, from covering sex-trait modification services.

Updates to the Premium Adjustment Methodology. CMS further seeks to update the premium adjustment methodology, which is used to set several different coverage parameters, including maximum out-of-pocket cost-sharing (MOOP), premiums, and tax credits. By way of background, the current premium adjustment methodology took a more stable approach given the uncertainty of premiums during the end of the COVID-19 Public Health Emergency. Under the Proposed Rule, beginning in 2026, CMS is proposing using an adjusted private individual and group market health insurance premium measure. Such a change will likely cause an increase of MOOP and an increase in premiums.

Updating De Minimis Thresholds. Plans on the Exchange are considered bronze, silver, gold, and platinum based on their actuarial value – whereby bronze plans must cover 60% of an average enrollee’s costs, silver plans cover 70%, gold plans cover 80%, and platinum plans cover 90%. Insurers may offer a specific plan if it is within a “de minis range” of this target value – for example, insurers may offer bronze plans so long as the actuarial value is within +5% and -2% of 60%. Similarly, insurers can offer a silver, gold, and platinum plan, if its value is within +2/-2 percentage points. CMS proposes to change the de minimis ranges to +2/-4 percentage points for all individual and small group market plans subject to the actuarial value, except expanded bronze plans. Further, CMS seeks to include a de minims range of +1/-1 percentage points for income-based silver cost-share reduction plan variations (which was previously −0/+1 percentage points). In the Proposed Rule, CMS estimates that this proposal would decrease premiums by one percent; however, it is likely to reduce the APTCs available.

Evidentiary Standard for Terminating Agents and Brokers. The Proposed Rule seeks to revise the standard for the Department of Health and Human Services (HHS) to terminate for-cause agents, brokers, and web-brokers from the Federally-facilitated Exchange by adding a “preponderance of the evidence” standard of proof regarding issues of fact. HHS may terminate its agreements with agents, brokers, and web-brokers for-cause for instances of non-compliance, fraud, and abusive conduct. Currently, regulations do not indicate an evidentiary standard HHS must apply; instead, the regulation states that HHS may terminate “in HHS’s determination.” CMS states that this change would “improve transparency in the process of holding agents, brokers, and web-brokers accountable for compliance.”

Potential Impacts to Plans

This Proposed Rule will have a direct impact on enrollment in the Exchanges. By adding measures that will increase premiums, reduce APTCs, and increase the administrative burden of applying and verifying enrollment, CMS will in effect discourage enrollment and decrease the number of individuals eligible for enrollment. Further, the changing rules may specifically discourage younger and/or healthier individuals from enrolling. This decrease in enrollment, coupled with the expected decrease in enrollment due to the expiration of the enhanced subsidies, could threaten the stability of the ACA Marketplace in the long run.

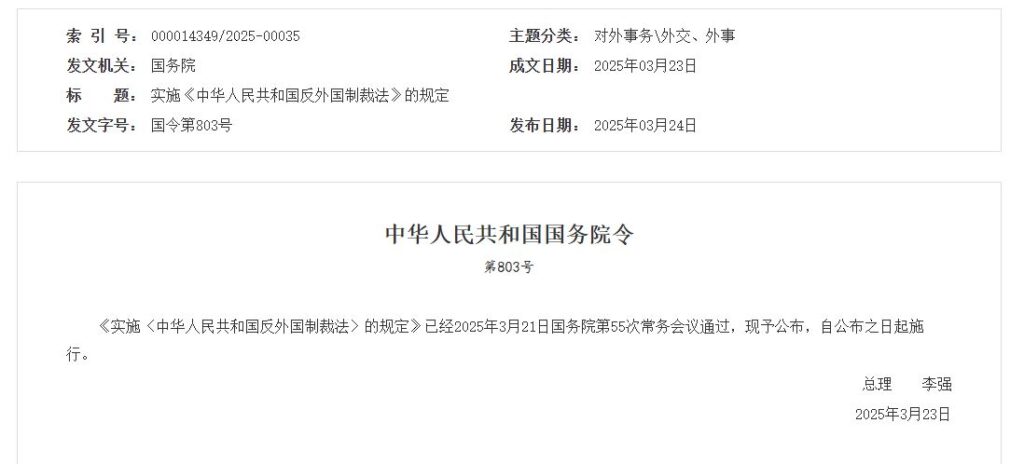

Regulations on the Implementation of the Anti-Foreign Sanctions Law of the People’s Republic of China – Foreign-Owned Intellectual Property Can Be Seized

On March 23, 2025, the State Council of the People’s Republic of China promulgated the Regulations on the Implementation of the Anti-Foreign Sanctions Law of the People’s Republic of China (实施〈中华人民共和国反外国制裁法〉的规定). Article 7 of the Regulations specifically allows for the seizure of intellectual property of those that “directly or indirectly participate in the drafting, decision-making, or implementation of the discriminatory restrictive measures in Article 3 of Anti-Foreign Sanctions Law.” Paragraph 2, Article 3 of the Law reads, “Where foreign nations violate international law and basic norms of international relations to contain or suppress our nation under any kind of pretext or based on the laws of those nations to employ discriminatory restrictive measures against our nation’s citizens or interfere with our nation’s internal affairs, our nation has the right to employ corresponding countermeasures.”

Article 7 of the Regulations reads:

The seizure, detention, and freezing referred to in Paragraph 2 of Article 6 of the Anti-Foreign Sanctions Law shall be implemented by the public security, finance, natural resources, transportation, customs, market supervision, financial management, intellectual property and other relevant departments of the State Council in accordance with their duties and powers.

Other types of property in Article 6, Paragraph 2 of the Anti-Foreign Sanctions Act include cash, bills, bank deposits, securities, fund shares, equity, intellectual property rights, accounts receivable and other property and property rights.

Relevant Articles of Law follow:

Article 3: The People’s Republic of China opposes hegemony and power politics and opposes any country’s interference in China’s internal affairs by any means and under any pretext.

Where foreign nations violate international law and basic norms of international relations to contain or suppress our nation under any kind of pretext or based on the laws of those nations to employ discriminatory restrictive measures against our nation’s citizens or interfere with our nation’s internal affairs, our nation has the right to employ corresponding countermeasures.

Article 4: The relevant departments of the State Council may decide to enter persons or organizations that directly or indirectly participate in the drafting, decision-making, or implementation of the discriminatory restrictive measures provided for in article 3 of this Law in a countermeasure list.

Article 5: In addition to the individuals and organizations listed on the countermeasure list in accordance with Article 4 of this Law, the relevant departments of the State Council may also decide to employ countermeasures against the following individuals and organizations:

(1) The spouses and immediate relatives of individuals listed on the countermeasure list;

(2) Senior managers or actual controllers of organizations included in the countermeasures list;

(3) Organizations in which individuals included in the countermeasure list serve as senior management;

(4) Organizations in which persons included in the countermeasure list are the actual controllers or participate in establishment and operations;

Article 6: In accordance with their respective duties and division of labor, the relevant departments of the State Council may decide to employ one or more of the following measures against the individuals and organizations provided for in Articles 4 and 5 of this Law, based on the actual situation:

(1) Not issuing visas, denying entry, canceling visas, or deportation;

(2) Sealing, seizing, or freezing movable property, real estate, and all other types of property within the [mainland] territory of our country;

(3) Prohibiting or restricting relevant transactions, cooperation, and other activities with organizations and individuals within the [mainland] territory of our country;

(4) Other necessary measures.

The full text of the Regulations is available here (Chinese only). A translation of the Anti-Foreign Sanctions Law is available from NPC Observer here.

Benefits Basics – When an Employee Dies: A Resource Guide for HR & Benefits Professionals

As a member of your company’s human resources or employee benefits department, one of the most difficult calls you may receive is from a colleague or an employee’s family member notifying you of the death of an employee. This situation demands you to be at your best – you will be called upon to usher your company’s workforce through the loss of a colleague and to help your HR department and grieving family members navigate many benefits and compensation issues that must be dealt with related to the deceased employee. This guide provides a high-level reference resource, in a plan-by-plan format, on how to approach each type of compensation or benefit arrangement when an employee dies, and offers up some practical tips on employee benefits issues that may come up as you manage your company’s compensation and benefit administration for a deceased employee.

The information given in this guide is general in nature and is not intended to address every benefit or tax issue that may come up when dealing with the death of an employee or other nuances that may arise when considering the deceased employee (or their specific family and probate situation) or the specifics of your company’s benefit plans. In addition, any tax or other rules described in this guide are current as of the date of this guide, and do not infer that the rules described are the only rules (tax or otherwise) that may apply and are subject to change. As a result, we always recommend that you engage your in-house or external legal counsel or other tax or employee benefits advisors when working through compensation and benefits issues related to the death of an employee.

An Overview of Relevant Law

Before we dive into discussing issues for administering your company’s compensation and benefit plans, it is important to have a high-level understanding of the probate process because, as we explain below, what happens in probate can affect who is entitled to certain death benefits. In addition, it helps to understand how the Employee Retirement Income Security Act (ERISA), a federal law governing most retirement and welfare benefit plans, interacts with state laws when death benefits are involved.

Overview of Probate

“Probate”is the legal process through which a court appoints an executor (in some states, called a personal representative) to administer the deceased employee’s estate, and validates a will (if there is one) or decides who inherits the deceased’s estate if there is no will. If the deceased had a will, that document would normally name one or more individuals to serve as the executor of the estate. If the employee dies without a will, then state law provides a list of people who are eligible to fill the role.

A court will ultimately appoint one or more individuals to serve as executor for the deceased employee’s estate, by issuing “Letters of Administration”, “Domiciliary Letters” or simply “Letters”, which give the executor authority to act. (Other terms might also apply to the form of the document used for this appointment.)

However, there are two times when probate may not be needed to determine who has the right to a deceased employee’s outstanding compensation or benefits:

Beneficiary Designations. If the deceased employee has arranged for their assets to pass directly to one or more beneficiaries without going through the probate process, then these items are not counted as part of the probate estate. In the employee benefits context, this would occur when an employee has made beneficiary designations related to a benefit. Thus, if your company’s compensation or benefit plan has a beneficiary designation process that was utilized by the employee, then waiting for the probate process is generally not needed in order to distribute death benefits. This is why it’s important for employer compensation and benefit plans to permit (and encourage the use of) beneficiary designations—it helps employees (especially executives) in their estate planning process and may allow the employee’s accrued benefits to pass directly to their beneficiaries without the hassle and delay of probate.

Small Estate Affidavit. If the value of the deceased employee’s estate is below the dollar threshold set by state law, then the employee’s heirs may be able to use a “small estate affidavit.” This allows heirs to receive the employee’s assets without having to go through probate at all (or permits an expedited probate). In other words, if you receive a small estate affidavit, any payments owed to the deceased’s estate instead are paid directly to the heir(s) listed in the affidavit.

Interaction of ERISA and State Laws

ERISA Section 514(a) explicitly preempts state laws that “relate to” an employee benefit plan that is subject to ERISA, with limited exceptions for certain insurance, banking, and securities laws. Courts have interpreted this preemption language to mean that any state law that refers directly to an employee benefit plan, or that bears indirectly on an employee benefit plan, is not enforceable against an ERISA-governed employee benefit plan. For example, if an ERISA benefit plan says that a death benefit should be paid to a spouse, but state law says that the death benefit under a benefit plan should be paid to the estate, then the terms of the plan will control instead of the state law. The U.S. Supreme Court confirmed this approach in their 2001 opinion in Egelhoff v. Egelhoff (ERISA preempts a state law that revokes beneficiary designations upon divorce). Similarly, in their 2009 opinion in Kennedy v. Plan Administrator for DuPont Savings & Investment Plan, the U.S. Supreme Court held that a plan may rely solely on its plan documents to determine the proper beneficiary for a death benefit, and can ignore extraneous documents that contradict the terms of the plan (such as a divorce decree).

What does this mean for you when administering benefit plans?

Where an ERISA plan is involved, you need only look at the terms of the plan (including any beneficiary designations, if applicable under that plan) to determine who is owed payments or benefits following an employee’s death.

But, for non-ERISA plans, the result is less clear. In that case, you would have to look to relevant state law to determine the extent to which you can honor any beneficiary designation. For example, many states provide that upon divorce, any beneficiary designation naming the ex-spouse as the beneficiary is automatically void, unless the divorce decree provides otherwise. For ERISA plans, you ignore that rule because ERISA preempts that state law and would implement the most recent beneficiary designation. For non-ERISA plans, however, if the deceased employee had named his spouse as the beneficiary, and then they divorced, you should generally void that beneficiary designation if required under state law.

A QUICK NOTE ON ERISA VS. NON-ERISA PLANS

Determining whether a benefit plan is covered by ERISA can be complicated. While your company’s most common broad-based retirement and welfare benefit plans, such as 401(k) plans, pension plans, and medical, dental, vision or other welfare benefits, will most likely be governed by ERISA, there are many nuances in the rules that exempt certain benefit plans depending on how the plan is structured. This issue commonly comes up with certain disability or severance benefits or policies. Bonus programs, deferred compensation plans or other voluntary benefits or payroll practices are usually not subject to the ERISA preemption rules. However, due to the complexity of these rules, if you are unsure whether a benefit program is an ERISA or non-ERISA plan, consult with your benefit plan advisors when deciding whether to allow beneficiary designations.

Practical Steps to Take When an Employee Dies

Who You Should Involve

If you receive the initial call about an employee’s death from a family member, it’s imperative that you promptly contact the following individuals within your organization: the head of HR for the employee’s business unit (who should, in turn, contact the deceased’s manager and co-workers), the payroll department, the equity administration team (if any), the compensation team (if any), and all relevant members of the employee benefits team. You may also need to tell your financial or accounting department if the deceased employee has significant amounts of unvested compensation that will vest or need to be paid due to their death. Each individual will play an important part in the weeks (and sometime months or years) to come.

After you’ve surveyed the plans and arrangements in which the deceased participated, you should also contact the relevant plan vendors or third-party administrators, if there is one, who may need to take certain actions to account for the death of the participant.

While not a topic of this guide, work with your HR team (and the deceased’s family) to determine the appropriate format and contents of any messaging to your broader workforce, and possibly even customers or other suppliers, about the employee’s death.

NOTE ON COMMUNICATIONS ABOUT BENEFITS

When an employee dies, there are a significant number of people outside the company’s HR department who will need to be involved in communications related to the deceased’s compensation and benefits or who may inquire about benefits with the HR team, including the executor, family members and other potential beneficiaries. Therefore, remember to be mindful about who is actually entitled to receive communications or information about each type of benefit, depending on the terms of the plan, who is the designated beneficiary, or who is the person authorized to represent the deceased’s estate. And, ensure that you get any necessary documentation identifying who the company or the plan is authorized to speak with on a matter related to the deceased’s benefits before providing detailed benefit information. Consider designating a single point person on the company’s HR team to handle communications related to the deceased’s benefits to maintain consistency throughout the process.

The Information You Need

There are three documents you should get from the executor or deceased’s family or beneficiaries before taking any steps relating to compensation and benefits:

A copy of the death certificate. Not only will this prove the employee’s death, but will provide some important information, such as whether the employee was married, and will be required documentation for processing certain benefits.

Either a copy of the “Letters of Administration”, or simply “Letters”, which is issued by a probate court and names the executor(s) or a copy of a properly completed “small estate affidavit.” This document will let you know who you are authorized to deal with regarding any compensation or benefits for which there is no beneficiary designation on file.

A Form W-9 from the executor regarding the estate or from each heir listed in a small estate affidavit, as well as from any family member or beneficiary entitled to benefits or payments (as described below). The information on the Form W-9 will give your payroll department and your benefit plan administrators the information they need to make sure payments are properly reported to the IRS and state taxing authorities.

You will also need to figure out which benefit plans or programs the employee was enrolled in or otherwise had an accrued benefit under, and whether the employee had any individual agreements in effect with the company (such as equity awards, employment agreements, employee loans, etc.) and make sure you have copies of all of those documents and, if applicable, any beneficiary designations made by the employee. This information may come from internal HR records or from third-party benefit plan administrators or vendors. You also need to determine whether or not the plan in question is governed by ERISA, because as discussed above under “An Overview of Relevant Law”, and as explained below, for non-ERISA plans you may have to review state law to determine who is owed the payment or benefit.

Cash and Equity Arrangements

Overview

When an employee dies, you will need to consider the impact on a variety of compensation amounts or equity benefits. First, you should survey all of the cash and equity compensation that is or may be due with respect to the deceased. Almost certainly, a final paycheck will be due. Also consider:

Does the deceased have any outstanding paychecks that were issued, but not yet cashed as of the date of death?

Does the deceased have accrued vacation or other PTO that may need to be paid based on applicable state law and the company’s PTO policies?

Does the deceased have business expenses that were incurred or submitted to the company, but have not yet been reimbursed?

Does any annual or long-term cash bonus plan provide for a payout upon death, and if so, when? (Bonus plans sometimes will pay out automatically at target upon death, or may provide for payout to occur at the end of the performance period based on the level of achievement of actual performance, and either on a pro-rated basis or in full.)

Are there commissions payable?

Is there an employment agreement that provides for payments upon death?

Does the deceased have equity awards, such as stock options or restricted stock units?

Is there an amount held in an employee stock purchase plan account for the deceased that was waiting to be used to buy employer stock?

On the flip side, does the deceased owe any money to the company, such as under a personal loan? And if so, do the terms of the loan permit the company to offset the loan amount from other compensation?

Second, after identifying the agreements, policies and arrangements under which cash or equity compensation may be due, determine whether the agreement, policy or arrangement is subject to ERISA. If you are unsure, consult with your legal or other benefits advisors on this point.

If it is subject to ERISA, then follow the death benefit payment provisions of the plan, if any. Because ERISA preempts state law, you are permitted to pay according to the terms of the plan, including the beneficiary designation on file for a plan that permits beneficiary designations.

If it is not subject to ERISA, then you need to check whether the program permitted a beneficiary designation (and if so, is a beneficiary designation on file) or whether the terms of the program provided for a default beneficiary, such as a spouse. If so, you need to check relevant state laws to make sure the beneficiary designation or the default provision can be honored. As discussed under “Interaction of ERISA and State Laws”, above, some state laws may override the beneficiary designation or program terms and require you to make payment as required by law, and not as described in your documents.

If the program is silent about beneficiaries, then check whether the state in which the employee worked has a wage payment law that would dictate to whom the compensation items listed above should be paid. If there is no law on point, then the executor of the employee’s estate or the heirs listed in a small estate affidavit, whichever is applicable, are entitled to the payments or equity.

Manner of Payment and Taxation

Any compensation paid to the executor of an estate should be made payable to “[Name of Executor], Executor, Estate of [Name of Employee]” or simply to “Estate of [Name of Employee]” or a similar variation of this. Any compensation paid to the deceased’s heirs under a small estate affidavit should be divided among the named heirs and paid directly to each of them.

For wages paid to the estate, heirs, or beneficiaries during the year when the employee dies, you must withhold FICA (both Social Security and Medicare taxes) and FUTA (federal unemployment taxes) on the payment and report the amount only as wages on the deceased employee’s Form W-2, Box 3 (social security wages) and Box 5 (Medicare wages) issued for the year of death. The FICA and FUTA taxes withheld are reported in Boxes 4 and 6, respectively. But, you do not report the payments in box 1 of Form W-2, and you do not withhold regular federal income taxes. If you make the payments after the year of death, then those payments are not reported on a Form W-2, and you would withhold no taxes.

Whether the payment is made in the year of death or after, you also report the payments made to the estate, heirs, or beneficiaries on a Form 1099-MISC in box 3. In general, no federal income tax withholding is required, although backup withholding rules may apply to these payments if the recipient fails to provide you with the taxpayer ID number or Social Security number for processing payments.

You should always work closely with your payroll department and related tax teams to determine the appropriate tax withholding and reporting for any payments related to a deceased employee’s compensation or equity arrangements.

Special Issues for Equity Awards

Vesting and Transfer of Equity Awards. For all types of equity awards, you will need to determine what happens to unvested awards upon the employee’s death, e.g., is the award forfeited, does vesting accelerate, or does vesting continue after death? How to treat any equity awards after the employee’s death will either be discussed in the equity plan document or in the award agreement issued to the employee at the time of grant. Sometimes, an employment agreement might also describe what happens to equity awards upon death.

If the employee has outstanding stock options, you also need to determine the post-death exercise period for those options. Again, this information should be available in the equity plan document, individual award agreement or possibly in an employment agreement. Inform the deceased’s beneficiary, estate, or heirs, as applicable, of how long they have to exercise the award after the deceased’s death under the terms of the plan or the award agreement and provide them information on how to exercise such awards. In addition, notify the third party administer for your equity plan (if any), of the deceased’s death and specify any actions they need to take regarding such employee’s awards.

Tax Treatment of Equity Awards. Similar to other types of compensation as discussed above, there is no required income tax withholding for any equity award transactions that occur after the deceased’s death. Rather, any compensation income recognized for this transaction should be reported on a Form 1099-MISC issued to the employee’s beneficiary, estate, or heirs.

FICA and FUTA tax implications for equity awards upon an employee’s death are more complicated:

FICA and FUTA tax withholding applies (and should be reported on the employee’s final Form W-2) for any awards that were (1) vested before the deceased’s death (not awards that vest because of the deceased’s death), and (2) were exercised/settled before the end of the calendar year of the deceased’s death.

FICA and FUTA tax withholding does not apply, however, for (1) any awards (or any part of an award) for which vesting is accelerated upon the deceased’s death, no matter when exercised/settled, and (2) awards exercised or settled after the calendar year in which the deceased’s death occurs.

Employee Benefit Plans

Qualified Retirement Plans

401(k) and Other Types of Defined Contribution Retirement Plans. 401(k) plans are the most common employer-provided retirement benefit offered to employees. If an employee dies with an account balance in a 401(k) plan, the first issue is to determine if the deceased employee was vested in his plan benefit at the time of death, and if not, whether the plan provides for full vesting upon death while employed (which is almost always the case). Also check the plan terms to see if any employer contribution (matching, profit sharing, or other non-elective contribution) is due to the employee for the year of death. While some plans may require that an employee normally be employed on December 31 or have completed 1,000 hours of service during the year to receive an employer contribution, those requirements are often waived if the employee dies while employed. You will need to review the 401(k) plan document and the summary plan description to determine what rules should apply to the employee’s 401(k) plan account. You should always also work with the plan’s recordkeeper to review the deceased’s account information to determine that the proper vesting calculations are applied to the account.

If there is a vested account, and if the participant is married at the time of death, then the laws governing defined contribution retirement plans require that the participant’s spouse automatically be the beneficiary of the account, unless that spouse has waived his or her right to be the beneficiary. A spouse waives their right to be the beneficiary if the participant has properly completed a beneficiary designation form naming another person(s) as the beneficiary, the spouse has signed that form, and the spouse’s signature is witnessed by a notary public or plan representative. In such a case, the vested account belongs to the named beneficiary, not the spouse.

If the participant is unmarried and there is no beneficiary designation on file, then the plan’s terms will dictate who is treated as the beneficiary. Plans often list family members in a certain order, such as children, then parents, then brothers and sisters, and so on. Ultimately, a plan will almost always indicate that the last beneficiary, if there are no others, will be the employee’s estate.

Once you have determined who is the proper recipient of the plan account balance, notify the individual (or the executor, if it’s the estate) that they have the right to the benefit and give them a copy of the plan’s summary plan description, so they understand when and how they may apply for benefits to commence.

In general, 401(k) plans let a beneficiary keep the 401(k) account in the plan, roll the account over (including directly to avoid withholding) to another qualified employer plan or an individual retirement account (IRA), or receive a distribution as a lump sum. Some defined contribution plans also offer distributions as installment payments or an annuity. A spouse beneficiary has the same rollover options that the employee would have had – i.e., take a distribution or roll over the distribution to an IRA or an employer qualified plan in which the spouse participates. A non-spousal beneficiary can also elect a rollover, but only to an IRA. See below for a “Warning” about how payments made to an estate are not eligible for rollover.

Under Internal Revenue Code rules governing minimum required distributions, if the beneficiary does not begin to receive distributions over a period not to exceed their life expectancy by December 31 of the year after the participant’s death (or for a spouse beneficiary, by December 31 of the year in which the participant would have attained their minimum required distribution age), then the entire account generally must be paid to the beneficiary by December 31 of the year containing the 10th anniversary of the participant’s death. Different rules apply if there is no beneficiary, such as if the payment is owed to the estate; in that case, distribution must be completed within 5 calendar years after the year of the employee’s death. It is important to note that while a plan may not pay benefits later than these dates, the terms of the plan may require that the payments be made earlier, and there are other nuances under the minimum required distribution rules that may apply depending on the facts of the particular employee and beneficiary. You should check the terms of the plan and consult with your plan recordkeeper to determine when benefits must be paid to a beneficiary or to the employee’s estate.

Pension Plans. While pension plans are becoming less common as each year goes by, many employers still maintain them, even though the benefits under the plan have almost all been frozen at this point. The following discussion assumes that the employee has not commenced their pension benefit at the time of death; if they did, then whether any death benefit is payable depends on the form of payment selected by the employee at the time benefits commenced (e.g., a joint & survivor annuity, term certain annuity, etc.). Since most pension plans do not permit employees to begin their pension benefits while employed (in no small part because the law generally does not allow it), the rest of this section assumes that the employee had not started to receive their pension benefits at the time of death.

The first issue to consider is whether the deceased employee was vested in their plan benefit at the time of death, and if not, whether the plan provides for full vesting upon death. If the deceased has a vested benefit under the plan, then the law requires that the pension plan pay a death benefit to the participant’s spouse. This type of spousal death benefit is known as a “qualified preretirement survivor annuity” or “QPSA”. There are two circumstances when a QPSA may not be payable, even if the participant is married at the time of death: (i) often, a plan will require that the participant and spouse be married for the one-year period preceding death for the spouse to be entitled to the benefit, and (ii) although rare, a plan may have allowed the participant to waive the QPSA to avoid having a deduction applied to their benefit to “pay for” the QPSA protection. You will need to review the plan documents and coordinate with the plan’s recordkeeper to determine what result will apply in the circumstance and if a QPSA benefit is due to a spouse.

While in the typical pension plan situation, no death benefits are payable if the deceased is unmarried (or was not married for at least one year), that is not always the case. Some pension plans that describe their benefits as a hypothetical account balance or as a lump sum—such as cash balance or pension equity plans—may provide for the full lump sum benefit under the plan to be paid to the surviving spouse, to the beneficiary designated by the participant, or if none, then to the estate. If the participant named a beneficiary and was married at the time of death, then the beneficiary designation is void if the spouse had not consented to the beneficiary designation as mentioned under “401(k) and Other Types of Defined Contribution Plans”, above. If the beneficiary designation is void, then typically the spouse would have the right to any death benefit.

Payment to the spouse, beneficiary or estate will be made at the time, and in the form, described in the plan document. Once you have determined who is the proper recipient of the death benefit, notify the individual (or the executor, if it’s the estate) that they have the right to the benefit and give them a copy of the plan’s summary plan description, so they understand when and how they may apply for benefits to commence.

A WARNING ABOUT PLAN PAYMENTS TO ESTATES (INCLUDING SMALL ESTATE AFFIDAVITS)

Any distributions paid to the executor of an estate should be made payable to “[Name of Executor], as Executor of Estate of [Name of Employee]” or simply to “Estate of [Name of Employee]” (or a similar variation). Note that your plan recordkeeper may have alternate ways of designating the recipient when an estate is involved. Any distributions paid to the deceased’s heirs under a small estate affidavit should be divided among the named heirs and paid directly to each of them. While the IRS rules normally allow beneficiaries to elect to rollover a qualified plan death benefit to an IRA (to avoid withholding taxes on the distribution), neither an estate nor the heirs listed in a small estate affidavit can elect a rollover distribution. Therefore, you will need to work with your plan recordkeeper to ensure that if death benefits are paid directly to individuals via a small estate affidavit, then those benefits are not permitted to be rolled over into an IRA.

Welfare Plans