Executive Use of Corporate Aircraft: Navigating Tax, SEC Disclosure and Other Key Considerations

Companies are increasingly allowing their chief executive officers and, in certain circumstances, other executives to use corporate jets (which may be chartered flights or fractionally or fully owned aircraft) for personal use due to various reasons. Although this benefit may be a relatively small percentage of an executive’s overall compensation package, it is still likely significant to the executive and may assist companies in attracting and retaining top talent. Further, commercial travel can pose security risks for high-profile executives; some companies permit these executives to use corporate jets due to safety and privacy concerns. Lastly, flying private may allow executives to save time and work more productively while traveling. For example, while traveling for personal reasons, executives may be able to conduct meetings and attend to any pressing business matters that arise mid-flight.

Despite these benefits, executive use of corporate jets may have complex implications, including tax consequences, SEC disclosure (publicly traded companies only) and other key considerations. As discussed in a separate Proskauer blog post, the IRS also recently announced a new audit campaign targeting the use of corporate jets, although it is unclear whether this will remain a focus of the new administration.

Tax Considerations for Private and Public Companies

Private and public companies, including private equity sponsors and other investment managers, and their employees must consider the tax consequences of allowing an executive or investment professional to use corporate jets for personal use. Specifically, under IRS rules, the value of an executive’s personal use of a corporate aircraft is treated as imputed income to the executive and is taxable compensation, subject to tax reporting and withholding. The most common method for calculating the value of the imputed income is by using the Standard Industry Fare Level (SIFL) method, which is based, among other things, on the distance flown, aircraft weight and number of passengers on a private jet. The value calculated under the SIFL method is reported as W-2 income to the executive and is subject to payroll taxes, although this amount is often significantly less than the fair market value of the benefits provided to the executive or the actual cost to the company of operating the jet. Additionally, although an employer’s cost of operating a non-commercial aircraft is generally deductible as an ordinary business expense, employers may not be able to deduct any entertainment expenses associated with personal travel under the Tax Cuts and Jobs Act (TCJA).

In order to determine the potential tax consequences of allowing an executive to use a corporate jet for personal use, companies must separately evaluate whether each passenger on a corporate jet is flying for a valid business purpose (e.g., while an executive may have a valid business purpose for flying on a corporate jet, the executive’s spouse may be traveling for entertainment in certain circumstances). If certain passengers (but not others) are traveling for entertainment, the portion of flight expenses allocated to those guests traveling for entertainment may be considered a taxable fringe benefit to the executive hosting the guests and, as an entertainment-related expense, may not be deductible to the employer under the TCJA. Importantly, these tax implications would apply even if a corporate jet has empty seats available for use at no additional cost.

SEC Disclosure Obligations for Public Companies

In addition to the foregoing tax implications, with respect to public companies only, personal use of company aircraft by the company’s named executive officers (NEOs) must also be disclosed in the company’s proxy statement under SEC rules. In particular, Item 402 of Regulation S-K requires disclosure of perquisites and other personal benefits if the total value exceeds $10,000 in a fiscal year. Importantly, the incremental cost to the company of providing this benefit, and not the value imputed to the executive, is used for purposes of this disclosure. As a result, this disclosure typically includes the cost of fuel, maintenance of the aircraft, crew costs, landing fees and in-flight catering and services, although fixed costs like the depreciation of the aircraft or any base salaries paid to staff generally are not required to be disclosed unless these costs are increased due to the executive’s personal use. In addition, if any single perk exceeds the greater of $25,000 or 10% of total perks, its specific value must be itemized, which may result in increased scrutiny from investors and regulators.

Other Key Considerations

In addition to the tax and SEC disclosure considerations, other key considerations should be analyzed. For example, internal policies and recordkeeping procedures should be established and monitored and, from a corporate governance perspective, appropriate approvals from the board or its committees (e.g., audit or compensation) should be obtained. Once approved, periodic reporting and monitoring may be advisable. Further, other regulatory considerations should be reviewed, particularly, where corporate-owned aircraft is used (e.g., FAA rules).

Proskauer Perspectives

Given these considerations, companies that permit executives to use their private aircraft should carefully track and retain information relating to their use. It is also best practice for companies to establish clear policies and guidelines regarding using aircraft for personal travel, including the process for obtaining pre-approval for any personal use. A company’s finance, tax, legal and human resources functions should also coordinate to ensure an executive’s imputed income is correctly tracked and reported and any personal use by an executive is properly disclosed in accordance with the SEC disclosure rules. Companies may also consider requiring executives to reimburse them for the costs associated with any personal use, which may mitigate some of the issues discussed in this blog post.

Although allowing executives to use a company’s private aircraft can be an attractive benefit for executives, businesses should proactively manage any associated tax, governance and operational issues and, for public companies, SEC disclosure obligations as well. By addressing these issues in a thoughtful and comprehensive manner, companies can support their management team by avoiding unnecessary surprise tax consequences and also reinforce investor confidence through consistent governance practices that contribute to long-term corporate stability and trust.

Reconciliation Bill Provisions Targeting Tax-Exempt Organizations Affect Hospitals

The budget reconciliation bill passed by the House of Representatives on May 22, 2025 (the “Reconciliation Bill”), contains a number of provisions targeting tax-exempt entities. While these provisions do not specifically target or call out hospitals, they may apply to tax-exempt and government hospitals.

Excise Tax on Compensation Expanded

Under current law, tax-exempt organizations and certain government entities are subject to a 21 percent excise tax on employee compensation that exceeds $1 million or that constitutes an excess parachute payment. The excise tax applies to amounts paid to the five highest compensated employees of the organization in the tax year and those who had been in that category since 2017 (“Covered Employees”).

Hospitals exempt from taxation under section 501(a) of the Internal Revenue Code of 1986 (the “Code”) and, in some cases, those owned by state or local governments are subject to this excise tax. However, compensation paid to licensed medical professionals for the performance of medical services does not count towards the $1 million trigger of the excise tax. Only the portion of a medical professional’s compensation for other services, such as research, teaching, or administrative or governance duties, are considered compensation for this purpose. Compensation paid by entities related to the tax-exempt or government entity, such as a for-profit or tax-exempt subsidiary or other affiliate, is included for this purpose.

Section 112020 of the Reconciliation Bill expands the scope of the excise tax by broadening the definition of Covered Employee to include all employees and former employees – not only those who are or have been one of the five most highly compensated. Tax-exempt and government hospitals entities and medical facilities affiliated with large hospital systems may be affected if they have large numbers of highly paid executives.

Tiered Increase on Private Foundation Investment Earnings

Hospitals, particularly those reliant on financial support from private foundations, also should be aware of the proposed increase in the tax on private foundation net investment income – as the increase will, potentially, leave private foundations with fewer assets to distribute to tax-exempt hospitals and other charities. Tax-exempt private foundations are currently subject to an excise tax of 1.39 percent on net investment income. Section 112022 of the Reconciliation Bill would increase the tax rate for private foundations with assets of $50 million or more. The increased rates will be tiered as follows:

2.78% if assets exceed $50 million but are less than $250 million;

5% if assets exceed $250 million but are less than $5 billion; and

10% if assets reach $5 billion.

Assets of related entities generally are included for this purposes — though assets will not be taken into account with respect to more than one private foundation. (The Reconciliation Bill does not address how assets will be divided when the aggregated group of related entities includes more than one private foundation.) Further, assets of related organizations that are not intended or available for the use or benefit of the private foundation are not taken into account unless the related organization is controlled by the private foundation. Notably, asset valuation would take on greater significance under a tiered system where a single dollar could double a private foundation’s tax rate. While the Reconciliation Bill states that asset value will be based on fair market value as of the close of the taxable year, numerous questions related to this calculation not addressed which may be problematic given that, if passed, this provisions will apply to taxable years beginning after the date of the enactment.

Parking and Transportation Benefits Included in UBTI

The Tax Cuts and Jobs Act, adopted in 2018, imposed the unrelated business income tax on parking and qualified transportation benefits provided to employees by tax-exempt employers. The provision was repealed retroactively the following year due to the complexity of calculating the amount to be included as unrelated business taxable income (“UBTI”) and uncertainty and confusion surrounding the application of the tax generally.

Section 112024 of the Reconciliation Bill would restore the requirement that tax-exempt organizations treat amounts paid and costs incurred to provide parking and qualified transportation benefits (defined in Code sections 132(f) and 132(f)(5)(C) respectively) as UBTI. Reinstating this requirement would increase the taxable income of tax-exempt hospitals and require them to update their accounting systems and administrative procedures to ensure compliance. As currently drafted, the provision does not address or resolve the complexities that led to its repeal in 2019.

Federal Court Strikes Down IEEPA Tariffs

On May 28, 2025, a three-judge panel of the U.S. Court of International Trade (CIT) unanimously struck down the extensive tariffs imposed by President Trump under the International Emergency Economic Powers Act (IEEPA). The CIT held that the imposition of the tariffs exceeded the authority granted to the President by Congress under IEEPA. The Court issued a permanent injunction blocking the administration from enforcing the IEEPA tariffs, and ordered the administration to issue the necessary administrative orders within 10 days to end them.

The affected tariffs are the 10% tariff on goods of most countries (referred to by the Court as the Worldwide and Retaliatory Tariffs), the 25% border tariffs on goods of Canada and Mexico in response to the illicit drug trade, and the 20% tariff on goods of China (together referred to by the Court as the Trafficking Tariffs). The affected Executive Orders (EOs) are as follows: 14257,[i] 14259,[ii] 14266,[iii] and 14298.[iv]

The government has appealed the case to the U.S. Court of Appeals for the Federal Circuit.

The CIT’s Ruling

In its opinion, the CIT emphasized that the U.S. Constitution expressly assigns the power to impose tariffs to Congress under Article I, Section 8, Clause 1, and that any grant of authority by Congress to the president to impose tariffs must be construed narrowly.

The Court held that IEEPA does not allow the Executive Branch to unilaterally impose tariffs without clear and bounded statutory authority. Instead, the Court read IEEPA as imposing two key limits on the tariffs:

Section 1702 of IEEPA, which permits the President to “regulate . . . importation,” must be construed narrowly. The Court examined the legislative history of this provision, which replaced a very broad grant of authority under the older Trading with the Enemy Act with a much narrower authority. The Court thus held that IEEPA does not authorize broad, unbounded tariffs like the Worldwide and Retaliatory Tariff Orders. The absence of “any identifiable limits” rendered these measures beyond the scope of the statute. Rather, the CIT determined that the Worldwide and Retaliatory Tariffs, which were imposed in response to the trade deficit, must conform within the limits of Section 122 of the Trade Act of 1974, the statutory authority that deals with remedies for balance-of payments deficits.

Section 1701(b) of IEEPA limits the President’s authority to actions that “deal with an unusual and extraordinary threat” and prohibits the use of IEEPA “for any other purpose.” The Trafficking Tariffs were implemented to encourage foreign countries to arrest or detain bad actors responsible for the flow of illicit drugs into the United States. The Court determined that the Trafficking Tariffs failed to satisfy the statutory threshold, because the tariffs do not bear a sufficient connection to the alleged threat to constitute “dealing with” the identified threat.

What’s Next

The CIT’s judgment permanently enjoined the IEEPA tariffs and ordered that within 10 days necessary administrative orders be issued to effectuate the permanent injunction.

The U.S. Department of Justice (DOJ) immediately appealed the ruling to the Federal Circuit Court of Appeals. The DOJ also submitted to the CIT a motion to stay enforcement of the judgment pending appeal. If the CIT grants the stay, the IEEPA tariffs would remain in place during the appeal.

If the CIT does not grant the stay, the DOJ will likely seek to stay the CIT’s permanent injunction in its appeal.

Importers should also note that the Trump Administration’s tariffs imposed under different statutory authorities (such as the duties on steel, aluminum, automobiles, and automobile parts issued pursuant to Section 232 of the Trade Expansion Act of 1962 and the duties on certain Chinese goods issued pursuant to Section 301 of the Trade Act of 1974) are not affected by the CIT’s ruling, and remain in effect.

We also note that even if its appeal is unsuccessful and the CIT’s order terminating the IEEPA tariffs is upheld, nothing stops the Trump Administration from pursuing more tariffs under Sections 122, 232, 301, or 338 of other relevant trade acts. We will continue to keep an eye on developments and keep you informed here.

FOOTNOTES

[i] Executive Order 14257, Regulating Imports With a Reciprocal Tariff to Rectify Trade Practices That Contribute to Large and Persistent Annual United States Goods Trade Deficits, 90 Fed. Reg. 15041 (Apr. 2, 2025).

[ii] Executive Order 14259, Amendment to Reciprocal Tariffs and Updated Duties as Applied to Low-Value Imports From the People’s Republic of China, 90 Fed. Reg. 15509 (Apr. 8, 2025).

[iii] Executive Order 14266, 90 Fed. Reg. at 15626 (raising China-specific duty rate from 84 to 125 percent effective April 10).

[iv] Executive Order 14298, Modifying Reciprocal Tariff Rates To Reflect Discussions With the People’s Republic of China, 90 Fed. Reg. 21831 (May 12, 2025).

Matthew Floyd contributed to this article

Federal Court Halts Broad Swath of Tariffs, Ruling Trump Lacks Authority Under IEEPA

On May 28, 2025 the little-known federal Court of International Trade issued its ruling in two challenges — one brought by 12 states attorneys general and one by private companies — to President Trump’s authority to issue tariffs using the International Emergency Economic Powers Act (IEEPA).

No prior president has used IEEPA to support tariffs, as IEEPA has historically been viewed as only a sanctions authority. In a unanimous per curiam opinion, the three-judge panel of the court invalidated using IEEPA to support tariffs under Article I, Section 8, clauses 1 and 3 of the Constitution, which assign to Congress “the exclusive powers to ‘lay and collect Taxes, Duties, Imposts, and Excises’ and to ‘regulate Commerce with foreign Nations.’”

After an extensive review of Congress’ delegation of trade authorities dating back to 1916, the court quotes IEEPA’s provision that its “authorities ‘may only be exercised to deal with an unusual and extraordinary threat with respect to which a national emergency has been declared… and may not be exercised for any other purpose.’” The court held that IEEPA does not delegate Congress’ power to the President “in the form of authority to impose unlimited tariffs on goods from nearly every country in the world.”

Concluding that IEEPA does not authorize any of the “Worldwide, Retaliatory, or Trafficking Tariff Orders,” the court found that narrowly tailored relief was inappropriate as “if the challenged Tariff Orders are unlawful as to Plaintiffs they are unlawful as to all.”

As a result, the challenged orders were permanently enjoined nationwide, allowing 10 calendar days for orders to be issued. The Trump Administration immediately filed for a motion to stay and appealed the order to the Court of Appeals for the Federal Circuit. The ruling halts the collection of the duties that were based on IEEPA under Executive Orders 14193, 14194, 14195 (the “Trafficking Tariffs”), and 14257 (the “Worldwide and Retaliatory Tariffs”) and all their amendments.

The “Trafficking Tariffs” are those imposed on Canada, Mexico, and China and the “Worldwide and Retaliatory Tariffs” are the global 10% ad valorem and the “reciprocal” global tariff schedule. It also reinstates de minimis treatment for shipments valued at less than $800. The ruling may also require refunding tariffs already paid.

Tariffs based on other authorities, including Section 232 tariffs on automobiles, aluminum, and steel, and Section 301 tariffs on China, remain in effect.

The ruling will likely throw a wrench into ongoing trade negotiations with dozens of countries, even while it is under appeal. In addition to the substantive ruling on IEEPA authority, both the nationwide injunction and the request for a stay pending appeal could make their way swiftly to the Supreme Court’s so-called “shadow docket” for emergency relief.

In addition, Congress may seek to ratify the tariffs, or the administration may seek to reinstate the tariffs using other delegated authorities. The ruling is unlikely to bring an end to the volatility that has surrounded the tariffs since they were imposed in April, and long-term planning around tariffs will continue to be challenging.

UK Cross-Government Review of Sanctions Implementation and Enforcement

On 15 May 2025, the UK government published a policy paper summarising findings from a cross-government review of sanctions implementation and enforcement. The Foreign, Commonwealth and Development Office led the review in collaboration with insights from external sanctions experts, as well as key sanctions departments and agencies, including HM Treasury, the Department for Business and Trade, the Department for Transport, HM Revenue and Customs (HMRC) and the National Crime Agency.

Anyone involved in advising on or implementing sanctions programs should take note of the content of these findings, as they illustrate where the United Kingdom’s sanctions implementation agencies will be focusing over the next few years.

The aim of the review was to identify further steps to improve and facilitate compliance, increase the deterrent effect of enforcement and invigorate the cross-government toolkit. The UK government has committed to implementing the review conclusions summarised below in the financial year 2025–2026:

Compliance

Targeted Guidance and Enhanced Outreach

The UK government will create additional guidance for, and increase engagement with, sectors with lower levels of sanctions awareness.

Engagement sessions conducted during the review highlighted variable levels of sanctions awareness within different sectors, with smaller businesses less able to access specialist advice.

Clearer and More Accessible Guidance

Sanctions guidance will be better organised, modern and searchable, with read across clearly signposted by posting comprehensive updates to sanctions pages and statutory guidance on GOV.UK.

Single Sanctions List

A single sanctions list incorporating the UK Sanctions List and the Consolidated List of Financial Sanctions Targets will be created. The list will aid industry in screening for designated persons, especially those targeted with non-financial designations, ensuring vital notifications do not go missed.

Ownership and Control

Guidance will be created to further clarify ownership and control obligations. Industry input highlighted the complexities of ownership and control determinations, involving complex due diligence and significant legal costs. Alignment with international partners on ownership will also be an area the UK government will focus on building.

Deterrence

Publication of Enforcement Information

It is vital that the consequences of sanction breaches are clear for effective deterrence. Sanctions enforcement actions will be published regularly for “teachable moments.”

Sanctions Enforcement Strategy

A government-wide sanctions enforcement strategy will be published to detail the range of enforcement outcomes available for non-compliance.

Penalty Settlement System

Currently, the United Kingdom does not have powers to agree to early settlements for sanctions cases beyond HMRC’s compound penalties. The UK government has committed to developing an early civil settlement scheme for breaches of financial sanctions.

Fast-Track Penalties

An accelerated civil penalty process for certain financial sanctions breaches will be developed to allow more resources and time to be given to the most complex, serious and deliberate of breaches.

Toolkit

Making It Easier to Report Suspected Breaches

Moving forward, reporting requirements will become clearer, with the potential for a single reporting point for suspected breaches. The aim is to avoid confusing reporting and potentially misdirected information.

Whistle-Blower Protections

Currently, to qualify for whistle-blower protection, a worker would need to make a disclosure to an employer, a legal advisor or a “prescribed person” under the Public Interest Disclosure (Prescribed Persons) Order 2014 (the Order). The UK government is committed to updating the Order to prescribe relevant government departments in relation to financial, transport and certain trade sanctions.

Future Commitments

The UK government has committed to exploring other areas to go further and deeper to improve sanctions enforcement and implementation depending on resourcing and emerging priorities.

Conclusion

These efforts aim to ensure the United Kingdom’s sanctions are robust, clear and effectively support foreign policy and national security goals.

Why the DOJ’s New Whistleblower Program Remains Relevant

On May 12, 2025, the U.S. Department of Justice (DOJ) issued a memorandum outlining the Criminal Division’s enforcement priorities and policies for prosecuting corporate and white-collar crimes in the new Administration. Later that week, Matthew R. Galeotti, head of the DOJ’s Criminal Division, addressed the new policies in a speech at the SIFMA Anti-Money Laundering and Financial Crimes Conference. Galeotti emphasized that the DOJ is “turning a new page on white-collar and corporate enforcement,” with a renewed focus on crimes that pose the greatest risk to U.S. interests. His remarks, coupled with the recent expansion of the DOJ’s Corporate Whistleblower Awards Pilot Program, signal a new era of accountability, transparency, and proactive compliance for portfolio companies operating in high-risk sectors.

Voluntary Self-Disclosure Policy – a Clear Path to Declination

The new policies include revisions to the Corporate Enforcement and Voluntary Self-Disclosure Policy (CEP). The revised CEP is designed to provide clearer guidance on the benefits of cooperation and a more predictable resolution process. Notably, companies that voluntarily self-disclose misconduct (in a “reasonably prompt” manner), fully cooperate, remediate appropriately and promptly, and have no aggravating circumstances will now receive a declination — not merely a presumption of a declination as previously offered. Moreover, a declination is still possible for cases with aggravating circumstances as prosecutors will have discretion to weigh the severity of those aggravating circumstances against the company’s cooperation and remediation efforts. Finally, the policy provides additional flexibility for companies that self-disclose in good faith where the government is already aware of the misconduct — such companies may still qualify for significant benefits, such as reduced fines and the avoidance of compliance monitors.

Expansion of the Whistleblower Pilot Program

While incentivizing self-reporting and cooperation, the new policies significantly broadened the scope of the Corporate Whistleblower Awards Pilot Program, announced in August 2024. Originally limited to violations by financial institutions, foreign and domestic corruption (including FCPA violations), and certain health care frauds, the program now covers a wider array of misconduct, including:

procurement and federal program fraud;

trade, tariff, and customs fraud;

violations of federal immigration law;

violations involving sanctions;

material support of foreign terrorist organizations, or those that facilitate cartels and transnational criminal organizations, including money laundering, narcotics, and Controlled Substances Act violations.

This expansion tracks the newly announced enforcement priorities and reflects the DOJ’s recognition that financial crime is often intertwined with broader threats to national security and global stability.

Competing Incentives for Whistleblowers and Companies

The financial incentives for whistleblowers who provide actionable information remain substantial. If a whistleblower provides information that leads to a successful forfeiture exceeding $1,000,000 in net proceeds, the whistleblower can receive up to 30% of the first $100 million in net forfeitures, and up to 5% of amounts between $100 million and $500 million.

At the same time, the incentives for companies to self-report a whistleblower complaint and still be eligible for a declination remain even stronger. Indeed, the Corporate Whistleblower Awards Pilot Program has an exception — if a whistleblower makes both an internal report to a company and a whistleblower submission to the Department, the company will still qualify for a presumption of a declination of charges under the CEP — even if the whistleblower submits to the Department before the company self discloses — provided that the company: (1) self-reports the conduct to the Department within 120 days after receiving the whistleblower’s internal report; and (2) meets the other requirements for voluntary self-disclosure and presumption of a declination under the policy.

What This Means for Companies

The message to corporate America is clear — compliance is a strategic imperative. Therefore, companies must:

Strengthen Internal Controls: Ensure compliance programs are tailored to the company’s risk profile and are actively monitored and updated.

Encourage Internal Reporting: Foster a culture where employees feel empowered to report concerns internally before going to regulators.

Review Investigation Protocols: Update internal investigation and remediation procedures to align with DOJ expectations.

Act Proactively: Voluntary self-disclosure and cooperation can significantly mitigate penalties and reputational damage.

Key Takeaways

The DOJ’s recent moves — both in policy and tone — reflect a maturing enforcement philosophy. Rather than wielding the stick indiscriminately, the Department is offering a clearer path for companies to do the right thing and receive the full benefits of cooperation. But the stakes remain high. With an expanded whistleblower program and a renewed focus on high-impact crimes, the cost of non-compliance has never been greater.

For portfolio companies willing to invest in integrity and transparency, the DOJ’s evolving framework offers not just protection — but opportunity.

Seetha Ramachandran, Nathan Schuur, Robert Sutton, Jonathan M. Weiss, William D. Dalsen, Adam L. Deming, Adam Farbiarz, and Hena M. Vora contributed to this article

US Easing of Sanctions on Syria Creates Opportunities and Risks

What Happened

On May 23, 2025, the US Department of Treasury Office of Foreign Assets Control (OFAC) issued a general license (GL 25) broadly authorizing financial transactions previously prohibited under the Syrian Sanctions Regulations (found at 31 C.F.R. part 542).

The Bottom Line

Effective immediately, GL 25 allows US persons to engage in certain transactions with the Government of Syria and certain blocked persons following almost 50 years of comprehensive economic sanctions on Syria, most of which were imposed during ex-Syrian President Bashar Assad’s rule. GL 25 represents the first step in lifting US sanctions on Syria. Companies and individuals seeking to do business with or in Syria should carefully consider the scope and limitations of GL 25. Companies should also review internal compliance policies, and sanctions compliance covenants and obligations, to take into account the shifting sanctions landscape with respect to Syria.

Full Story

US sanctions on Syria date from Syria’s 1979 invasion of Lebanon and expanded during Syria’s civil war through a range of legislative actions and executive orders. On January 6, 2025, following the end of President Bashar Assad’s rule, OFAC issued Syria General License 24, which authorized a narrow set of transactions with Syria’s transitional government and energy sector, as well as personal remittances. On May 13, 2025, President Trump announced that the United States would lift sanctions on Syria; on May 23, OFAC issued GL 25.

As described in the press release accompanying the issuance of GL 25, the license is intended to help rebuild Syria’s economy, financial sector and infrastructure; align Syria’s new government with US foreign policy interests; and bring new investment into Syria, signaling opportunity for companies interested in investing in the rebuilding of Syria.

GL 25 authorizes transactions that would otherwise be prohibited under the US economic sanctions on Syria, including new investment in Syria, the provision of financial and other services to Syria and transactions related to Syrian-origin petroleum or petroleum products. GL 25 also authorizes all transactions with the new Government of Syria, and with certain blocked persons identified in a list appended to the license (any transactions with other blocked persons not identified in the annex remain prohibited).

GL 25 represents a significant shift in the US sanctions landscape. For international financial institutions, the reach of US sanctions, especially the secondary sanctions imposed by the Caesar Act of 2019, have been a significant sanctions compliance concern. For nearly five decades, Syria has been viewed as a comprehensively sanctioned country, with the effect that financing and commercial documentation often specifically prohibits doing business in Syria.

The shifting sanctions landscape with respect to Syria introduces new compliance risks for companies seeking to do business there or otherwise take part in rebuilding opportunities. Although GL 25 represents a significant easing of sanctions—such that Syria can no longer be considered a truly “comprehensively” sanctioned country—it is important to note that issuance of the general license is merely an interim step intended to provide immediate relief. While certain sanctions can be lifted by executive order, other sanctions on Syria are imposed by statute and will require Congressional action. Syria’s re-entry into the global financial system may be complicated by this variation in different sanctions authorities as institutions begin to adjust to a post-sanctions Syria.

Financial institutions and companies should carefully review internal compliance policies to take into account the changing scope of sanctions on Syria. Companies and funds seeking to invest in Syria should also consider internal compliance policies with respect to Syria, as well as existing covenants in financing and other agreements that may restrict investment or other business dealings in Syria.

Washington State Expands Sales Tax, Increases B&O and Capital Gains Taxes

On May 20, Washington Gov. Bob Ferguson signed into law several bills aimed at closing Washington’s projected $16 billion budget gap, which were passed as part of 2025–27 operating budget.

Interested parties closely monitored the signing of these bills, especially SB 5814, which significantly expands Washington’s sales tax. The bill includes advertising services—generally digital—within the tax base, raising concerns from both in-state and out-of-state companies based on the lack of detail provided regarding the sourcing of such services. While the governor did not veto SB 5814, Washington legislators are aware of the concerns and additional action on this issue is expected.

Key Details of the Tax Changes Impacting Businesses and High-Net-Worth Individuals

Business and Occupation (B&O) Tax Changes: HB 2081 includes numerous B&O tax increases and modifies when the B&O investment deduction applies. This latter change was made in response to the Washington Supreme Court’s recent decision in Antio, LLC v. Dep’t of Revenue,1 essentially codifying the department’s position on that deduction. Notable B&O tax increases include:

–

A temporary 0.5% surcharge on a business’ taxable income in excess of $250 million beginning Jan. 1, 2026, and continuing through Dec. 31, 2029;

–

A permanent rate increase from 0.484% to 0.5% for certain categories of business activity (including manufacturing, wholesaling, and retailing) beginning Jan. 1, 2027;

–

A permanent rate increase from 1.75% to 2.1% for the services and other activities category for businesses with over $5 million in annual revenue beginning on Oct. 1, 2025;

–

A permanent rate increase from 1.2% to 1.5% for the financial institutions surcharge beginning on Oct. 1, 2025; and

–

A permanent rate increase from 1.22% to 7.5% for the advanced computing surcharge as well as an increase to the annual cap of $75 million beginning on Jan. 1, 2026.

Retail Sales Tax: SB 5418 expands the state sales tax to include many personal, business, and professional services, including digital advertising services, IT support, landscaping services, software training, tattoo services, data processing, website development, graphic design, temporary staffing services, and search engine marketing. SB 5418 also makes several modifications to Washington’s digital automated services provisions and provides that services between members of an affiliated group will be exempted. These changes are set to take effect Oct. 1 of this year.

Capital Gains Tax: SB 5813 creates a new capital gains tax top bracket of 9.9% for gains in excess of $1 million, retroactively applying from the beginning of this year (Jan. 1, 2025).

This is not an exhaustive list of all the changes that were made in conjunction with the state budget revisions but does reflect some of the key issues that may impact businesses and high-net-worth individual taxpayers. With the governor signing all of these bills, the Department of Revenue may begin to develop rules and policies on many of these new or expanded programs in the near future. Policy discussions may continue as cleanup legislation, and a special legislative session seems likely.

1 557 P.3d 672 (Wash. 2024).

Proposed Rule on Medicaid Tax Waivers: CMS Moves to Close a Loophole Shifting Costs to the Federal Government

On May 15, 2025, the Centers for Medicare & Medicaid Services (“CMS”) released a proposed rule, entitled “Preserving Medicaid Funding for Vulnerable Populations – Closing a Health Care-Related Tax Loophole” to address a financing loophole that allows states to shift more Medicaid costs to the federal government than intended (the “Proposed Rule”). If finalized as proposed, states that received CMS-approved waivers for state healthcare-related taxes within the last year—including California, New York, Michigan, and Massachusetts—would be required to modify or eliminate those state taxes immediately or risk losing federal matching funds for expenditures paid using those tax revenues. Comments from stakeholders are due by July 14, 2025.

The major policy change in the Proposed Rule would eliminate an existing waiver process that allows states to obtain approval from CMS for certain health care-related taxes, which seven states, including California, New York, Michigan, and Massachusetts, have relied on to finance their share of Medicaid costs.

Under existing federal law and regulations, when a state imposes a tax on healthcare providers and uses the revenue to support Medicaid payments, the federal government provides matching funds, so long as the tax complies with specific statutory requirements set forth by Section 1903(w) of the Social Security Act.

To ensure that states are not simply recycling money back to taxed providers to draw down more federal funding, the law requires that health care-related taxes be broad-based, uniform, and not include “hold harmless” arrangements—where providers are effectively reimbursed for the taxes they pay. States can request a waiver from the “broad-based” and “uniform” requirements if they can show the tax is generally redistributive—i.e., it generally derives revenue from taxes on non-Medicaid services and uses them to finance the State’s share of Medicaid payments for services. Since 1993, CMS has used specific statistical tests to assess whether a waiver-eligible tax is generally redistributive.

However, CMS is concerned that states have found ways to structure their taxes that technically pass the statistical test for a waiver of the “uniformity” requirement, but that actually impose more of the tax burden on Medicaid services than non-Medicaid services—such as by imposing higher tax rates on Medicaid services than on commercial services—and therefore are not “generally redistributive.” CMS highlighted several examples of taxes imposed on managed care organizations (MCOs) where a disproportionate share of the tax burden is imposed on Medicaid member-months. CMS believes that these arrangements undermine the federal-state cost-sharing structure of Medicaid.

The Proposed Rule seeks to close this loophole by refining how CMS evaluates whether a health care-related tax is generally redistributive. It introduces more stringent requirements to ensure that taxes do not disproportionately target Medicaid providers and that the distribution of the tax burden reflects a true cross-section of the provider market. According to CMS, closing this loophole could save the federal government over $33 billion over five years.[1]

Specifically, CMS proposes to keep the two existing statistical tests for waivers of the broad-based and uniformity requirements, respectively, but to add new requirements that must be met even if the applicable statistical test(s) are satisfied. This represents a significant shift in CMS’s approach, moving from a focus on statistical form to economic substance. Under the Proposed Rule, a tax that meets the applicable statistical tests still is not “generally redistributive” and will not be approved by CMS if: (i) the tax rate imposed on any taxpayer or taxpayer group based on its Medicaid taxable-units is higher than the tax rate imposed on non-Medicaid taxable units (e.g., an MCO tax where Medicaid member months are taxed at $200 per member-month and non-Medicaid member months are taxed at $20 per member month; (ii) the tax rate imposed on a taxpayer or taxpayer group that is defined based on its Medicaid volume or percentage is lower for the lower-Medicaid volume group and higher for the higher-Medicaid volume group (e.g., a higher tax rate for nursing facilities with a Medicaid inpatient utilization rate greater than 5% than the tax rate for nursing facilities with a Medicaid inpatient utilization rate less than 5%).

CMS explains that all seven of the existing approved State tax waivers would fail (i) and at least one existing State tax waiver would also fail (ii). CMS also proposes that any State tax that has the same effect as either (i) or (ii) – that is, where a State is using a substitute definition, measure, or attribute as a proxy for Medicaid to achieve the same effect—would not be generally redistributive and would not be approved.

To implement this change, CMS also proposes to define new terms for “Medicaid taxable unit” and “non-Medicaid taxable unit” to distinguish between units that the basis of Medicaid payment (like Medicaid bed-days, Medicaid revenues or Medicaid charges) or otherwise associated with the Medicaid program and units that are not associated with the Medicaid program. States may need to reassess how they define tax bases for taxpayers and classes of providers to ensure they do not disproportionately burden Medicaid utilization.

The Proposed Rule would provide a one-year transition period for any State tax that does not comply with the new requirements, but only if CMS approved the tax waiver more than two years prior to the effective date of any final rule. By contrast, state taxes that obtained waivers more recently (i.e., less than two years prior to the effective date of any final rule), such as California, Michigan, Massachusetts, and New York, would not be eligible for a transition period and would be required to comply with the new requirements as of the effective date of the final rule or risk a reduction in federal Medicaid funding.[2] With no transition period for recent waivers, states like New York may have as little as 60 days to comply after the final rule is published. States, their Medicaid agencies, and stakeholders should begin internal reviews now to avoid rushed changes to avoid losses in federal funding.

Date CMS Approved Waiver

Effective Date of Final Rule

Eligible for Transition Period?

State Fiscal Year Begins

Compliance Deadline

July 1, 2016

January 1, 2026

Yes

April 1

April 1, 2027*

July 1, 2016

February 1, 2026

Yes

January 1

January 1, 2028**

December 10, 2024

January 1, 2026

No

N/A

January 1, 2026

December 10, 2024

February 1, 2026

No

N/A

February 1, 2026

* Under existing regulations, a modified waiver package would need to be submitted to CMS for approval by June 30, 2027 to have a retroactive April 1, 2027 effective date. CMS is also considering a number of different alternatives for the transition period, including on the one hand, narrowing the availability of the transition period to state taxes with waivers approved more than three years prior to the effective date, and on the other hand, extending the transition period to one year for states with more recent tax waiver approvals (i.e., within the last two or three years) and two years for states with older tax waiver approvals.

States with recent waiver approvals, such as New York, California, Michigan, and Massachusetts, may need to act quickly to re-evaluate their existing tax structures. This may include identifying Medicaid-heavy tax metrics, engaging affected providers, and assessing whether changes in state laws or regulations related to state taxes are needed. CMS’s stated position that existing tax waivers do not meet the new requirements suggests that significant structural changes, not just technical adjustments, may be needed. States can no longer rely on prior approvals and may consider preparing now to modify their tax structures to meet the proposed requirements as of the effective date of any final rule.

Notably, this regulatory effort coincides with legislative activity in Congress on the same topic. On May 14, the House Energy and Commerce Committee advanced its portion of the fiscal year 2025 budget reconciliation bill, which includes multiple amendments to the Medicaid statute to limit states’ use of health care-related taxes. The Bill would impose a federal moratorium on new or increased provider taxes, and proposes to codify in the Medicaid statute conditions for when a health care-related tax is not “generally distributive.”[3] The conditions outlined in the bill are substantially similar to the conditions CMS included in the Proposed Rule. The bill also would authorize the Secretary to determine an appropriate transition period, not to exceed three fiscal years. If enacted by Congress later this summer, that may accelerate the time frames for compliance with the new requirements compared to the time required for CMS to consider submitted comments and finalize the Proposed Rule.

FOOTNOTES

[1] Preserving Medicaid Funding for Vulnerable Populations – Closing a Health Care-Related Tax Loophole Proposed Rule, Ctrs. For Medicare & Medicaid Servs. (May 12, 2025).

[2] Id.

[3] Comm. Print Providing for Reconciliation Pursuant to H. Con. Res. 14, Subtitle D—Health, § 44131, 44132,44134, 119th Cong. (2025).

Listen to this post

Tariffs & Supply Chains: An English Law Perspective on Contractual Levers You May Have (or Want)

These are challenging times for supply chains. In recent months, the US government has announced, reversed, delayed, adjusted, and enacted a series of tariffs on imports to the United States from a long list of countries; some countries have retaliated, and others are negotiating and beginning to announce trade deals. The supply chain is trying to adapt fast and frequently.

Whether tariffs are imposed for additional tax revenue, to encourage domestic production and consumption, as a geopolitical tool to favour some countries over others, a combination of these or otherwise, they are having significant impact. From increasing material and production costs, to squeezing operating margins, increasing administrative and trade compliance burdens, inflating end-product pricing, and affecting supply and demand cycles with stockpiling in advance of anticipated tariffs or import delays in case tariffs are soon to be removed or reduced.

While supply chain restructuring or diversification may be a medium or longer-term priority, its participants may wish to be agile and respond swiftly in the short-term, but where does the tariff burden lie, how flexible are the contracts, and what contractual levers might be available to mitigate the impact?

We consider below (from an English law perspective – though the comments may have general application) some contractual levers that may help navigate these challenges. One comment of universal application is that: whether any tariff announcement is sufficient to trigger a contractual lever, and the consequences which may flow from it, will be contract clause and context specific.

Where Does the Tariff Burden Lie?

Does the contract contain provisions which allocate the parties’ risks and responsibilities in the event of tariffs? If not, each party may bear the increased costs of performing their respective obligations.

Does a Tariff Trigger Automatic Consequences?

Dynamic pricing provisions may vary the price payable by reference to an underlying index, which may shift in response to a tariff, or they may build-in formulae to adjust prices by reference to an increase in the cost of supply, which could include the imposition of a tariff. These provisions may provide that price adjustments are time limited, subject to a maximum cap, or kick-in only once a cost threshold is exceeded.

What Contractual Levers Are Available?

Does the contract provide opportunities for the parties to require or request variations, to suspend performance, or even to terminate, in the event of tariffs or significant cost increases?

Surcharge

Surcharge pricing may allow a party to apply an additional fee beyond the original contract price, to cover a particular cost. End users will often be expected to pay increased prices for consumer goods affected by tariffs, and a similar principle may apply to business-to-business contracts if a clause permits a party to levy surcharges. As with dynamic pricing provisions mentioned above, these may be subject to threshold and time limits, and they may provide a unilateral right to adjust pricing, or trigger a renegotiation.

Change in Law

The contract may specify the consequences of a change in law after its execution. The clause would need to be examined to assess whether: a tariff could qualify as a change in law; it requires contractual adjustments or triggers a renegotiation; it allocates the consequent burden of additional cost of compliance; it addresses the ramifications of any delays caused, or even perhaps provides a right to terminate. Such a clause may only apply if the change in law requires that the contract be amended (for example, in order for it to remain compliant with the law that has changed), so whether a tariff could be said to require a variation or merely affect the economics of the arrangement could give rise to debate/dispute.

Force Majeure / Frustration

Is often the first thing that comes to mind when a significant event impacts a contract, but circumstances in which such a clause may be successfully utilised can be limited. There is no standalone doctrine of force majeure under English law, so step one is to see if there is such a clause. A force majeure clause is usually composed of two parts: the first lists a series of events considered to trigger the force majeure provisions, and the second determines the consequences, which may for example include a right to suspend performance temporarily and/or to give notice to terminate, if certain circumstances apply. Whether a tariff constitutes a force majeure event will depend on the clause wording.

Even if tariffs are specifically referenced, force majeure clauses can require that the triggering event make it legally or physically impossible to perform, rather than merely more expensive, and English caselaw indicates that such clauses will not generally be construed to extend to changes in economic circumstances. So, force majeure may not be an especially useful lever in respect of tariffs. That said, if the imposition of a tariff has knock-on consequences, such as a key component or ingredient becomes temporarily unavailable rendering it impossible to manufacture a product, there may be better prospects of force majeure responding to assist.

Absent a force majeure clause, parties to English law contracts sometimes consider the doctrine of frustration (discharging a contract when an unforeseen event makes the contract incapable of being performed), though the English courts have consistently held that increased costs or reduced profitability will not be sufficient to frustrate a contract – so unless the impact of a tariff is so extreme as to create impossibility, it is unlikely to assist.

MAC / Hardship

Is there a “material adverse change” (MAC) or a hardship provision? MAC clauses may allow a party (e.g. a buyer in an acquisition) to renegotiate or withdraw from a transaction if a certain event occurs which has a material negative impact. The potential applicability and effect of the clause would need careful consideration in each case. It may list specific triggering events, refer more generally to any matter which has a materially adverse effect, or incorporate carve-outs that may prevent tariffs from being considered a relevant event. What consequences are specified, and does it trigger a renegotiation or provide a right to terminate or withdraw?

Alternatively, there may be an economic hardship clause, permitting a party to trigger a renegotiation if something occurs making performance significantly more difficult / financially onerous (though not impossible). Carefully defining what constitutes “hardship” will be important, as this may be an area ripe for dispute when something drastic occurs. Hardship clauses are not especially common in English law contracts, though sometimes appear in cross-border long-term supply relationships, or where markets may be volatile.

Change Control / Variation

some longer-term or complex contracts may have a prescribed process to propose, evaluate, negotiate in good faith, and implement changes to contract economics following a change to the scope of work or a cost increase for example.

The boilerplate provisions in many contracts incorporate a variation clause expressly permitting contract amendment by agreement between the parties, and parties are generally free to agree and implement variations to their contracts in any event (subject to any express restrictions in the contract).

Their utility can be limited where they do not specify what changes should be made on the occurrence of a triggering event, constitute only an “agreement to agree”, or provide no more than an option to negotiate, though incorporating an obligation to negotiate in good faith may be more helpful than nothing at all. In certain circumstances (such as where the parties have a particularly strong desire to continue working together, or where all parties find themselves similarly impacted by an event), a mutually agreeable change control or variation clause may assist to achieve a commercial resolution. That being said, where a collaborative relationship persists despite challenging circumstances, the parties may elect to vary the underlying agreement regardless of any express variation process. It would be extremely unusual for a commercial agreement to prohibit its parties from amending the agreement in writing executed by all parties.

Termination

If nothing sufficiently reduces the damage that will be done by continuing to perform, looking at contract termination possibilities may be the only option.

Some of the provisions mentioned above may allow notice of termination to be given if certain circumstances have arisen. If not, does the contract permit termination for convenience by giving a period of notice? Where such a right exists, it may however be accompanied by exit costs and these should be balanced against the costs associated with the tariff to ascertain which route makes most economic sense. Or has the imposition of the tariff brought about a breach of the contract sufficiently serious to warrant a termination – for example, if the tariff brings about a failure to supply or a refusal to order, accept delivery or pay – whether under a provision allowing notice of termination to be given in the event of a material breach or under the common law for repudiatory breach?

Comment

Scope for complex contractual disputes abound: contrasting interpretations of contractual provisions; whether they are enforceable; whether a clause encompasses a particular event; whether that event has occurred; can US tariffs be classified as “unforeseen” events when they featured so prominently in the election campaign?; has a force majeure event occurred?; if so, has the obligation become impossible (not just expensive) to perform?; what constitutes a material adverse change or a hardship?; is a party engaging in negotiations in good faith?; has a right to terminate arisen?; whether the tariff has brought about a breach of contract; does a breach give rise to a right to terminate under the contract or English common law? And these are just a number of examples arising from the concepts considered above.

The firm’s Commercial Disputes and International Arbitration lawyers regularly assist clients seeking to rely on, or challenge an opponent’s reliance on, the types of levers discussed above, and with resolving any complex contractual disputes arising. The team works closely with our international trade team, which is advising our global clients in real-time as the trade landscape continues to shift.

We noted above that the availability and utility of these rights and levers will be contract clause and context specific, and the wording of each provision will be very important. Do your supply chain contracts include some or all of the levers you need, and will they operate as you would like?

There is a delicate balance to be struck between incorporating levers for sufficient flexibility and allowing the parties to navigate their business through unexpected and significant disruptive events (such as tariffs), whilst at the same time maintaining levels of contractual certainty that may be required to justify investment in a relationship, and so that everything is not forever up for renegotiation. Our commercial contracts and other lawyers assist clients to assess the context-specific strategic benefits of these levers, advising on the drafting, negotiation and incorporation of such provisions. Ultimately, it is about tailoring the balance between flexibility and certainty to the specific industry and business needs of our clients in order to future proof their commercial relationships.

Tariffs and Alcohol Production Contracts: The New Trade Landscape

Since early 2025, U.S. alcohol manufacturers have found themselves on the frontlines of a fresh wave of trade disruptions. With the “Liberation Day” tariffs, core inputs such as cans, bottles, grain, labels, barrels are seeing their prices rise. For producers using imported goods, relying on contract production, or alternating proprietorship relationships, these cost shifts are no longer theoretical.

Craft alcohol manufacturers operate on thin margins and often lack leverage in global supply chains. For years, flexible terms and handshake understandings filled the gaps. But in today’s trade environment, producers need to tighten up their contracts. This starts with how manufacturers manage tariff risk.

Force Majeure Provisions are Usually Inapplicable

It’s a common misconception that rising costs from tariffs are a “force majeure” event. They’re not. Force majeure covers “acts of God” such as hurricanes, pandemics, and labor strikes; the kinds of events that make performance impossible. Tariffs, by contrast, just make performance more expensive. Courts generally do not excuse a party from paying or performing because of an unfavorable cost shift. Unless your force majeure clause expressly covers tariffs or government duties (and most don’t), you’re on the hook. This is why producers need a different set of tools, and that comes through good contract drafting.

Tighten up Your Contracts

To keep your margins intact and your relationships healthy, you need proactive language that deals with tariffs head-on. Many producers are now reworking their contractual agreements like alternating proprietorships and contract production deals—to include specific language that allows for tariff surcharges. These provisions enable the host producer or manufacturer to pass on new tariffs as a separate line item. Other agreements use broader “change in law” provisions to trigger pricing adjustments if newly enacted duties or government actions materially alter production costs. These mechanisms function quite differently from general hardship or material adverse change (MAC) clauses. While hardship clauses typically permit renegotiation in response to unforeseen circumstances, they often lack enforceable standards. Without clear financial thresholds or defined triggers, a court may still enforce the original pricing. By contrast, tariff surcharges and change-in-law provisions directly allocate costs and give parties a reliable structure for managing increases without creating ambiguity.

Even simple contractual language can go a long way. For instance, a sentence reserving the right to apply a “tariff surcharge equal to any new or increased import duties imposed after the effective date” keeps pricing transparent and ensures both sides know where they stand. Likewise, a well-drafted change-in-law clause can provide a formal mechanism for renegotiating terms in response to legislative or administrative actions—such as executive orders or international trade measures—that impact the cost of inputs.

In the alternating proprietorship and contract brewing contexts, tariff risk deserves even more attention. These agreements often require the host to secure and purchase certain ingredients and materials used in production. That includes imported items like glass, barrels, malt, specialty grains, or fruit. If tariffs are imposed on these goods during the term of the agreement and the contract is silent, the host may be left to “eat” those additional costs. Sometimes these agreements allow only for annual cost increases. Given the volatility of the new tariff policies, that’s not a sustainable model. For this reason, these agreements should explicitly state that the host is permitted to pass along any new or increased import duties associated with ingredients or materials sourced on behalf of the tenant.

Tariffs may go up or down, but what shouldn’t fluctuate is your contract’s ability to handle them. Rather than reaching for force majeure clauses ill-suited to cost increases, producers should plan ahead by including express surcharge rights, price adjustment mechanisms, and change-in-law protections. This way, if tariff rates spike again, your production doesn’t grind to a halt — and neither does your profit margin.

Remember, well-drafted agreements don’t just assign risk; they preserve relationships. When the rules of trade change over a single tweet, the best defense is a well-drafted contract.

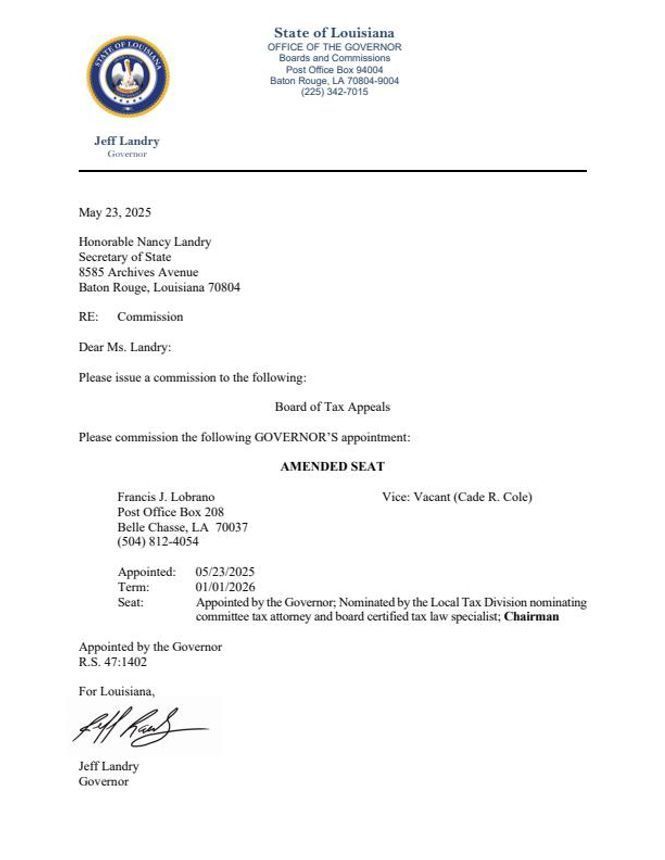

Judge Jay Lobrano Appointed Local Tax Judge at the Board of Tax Appeals

On May 23, 2025, Louisiana Governor Jeff Landry appointed Francis J. (Jay) Lobrano as the Local Tax Judge of the Louisiana Board of Tax Appeals to complete the term of outgoing Local Tax Judge, now Louisiana Supreme Court Justice Cade Cole.

Judge Lobrano has served as the Chairman of the Board since March of 2022, and has served as a member of the Board since April 2016. In his new role, Judge Lobrano will preside over all local tax matters pending at the Board, including sales and use tax disputes between Parish tax administrators and taxpayers, as well as legality challenges involving property tax assessments.

Judge Lobrano will still sit as the Chairman of the full Board, that hears tax matters involving state tax matters.

Open File0.17MB